Sophie Doyle, Financial Aged Care Specialist at Morgans Gosford said “Families are faced with many so many decisions when a loved one can no longer lived independently to move into permanent care.

One of the most common questions I get asked is “Do we have to sell the family home to fund Mum or Dad’s care?”

There is no simple answer to this question, as there are a number of factors to be considered. These include but are not limited to, the current value of the parent/s income and assets (including the family home).

Selling the home can result in the person’s aged pension being reduced, or stopped and possibly affect the aged care assets test. At the same time, keeping the home and renting it can also affect the age pension and assets test. Another considered when keeping the home is, does Land Tax apply?

When a person moves into residential aged care their home maybe left vacant or maybe rented and used as an investment property, and land tax may start to apply to the former home.

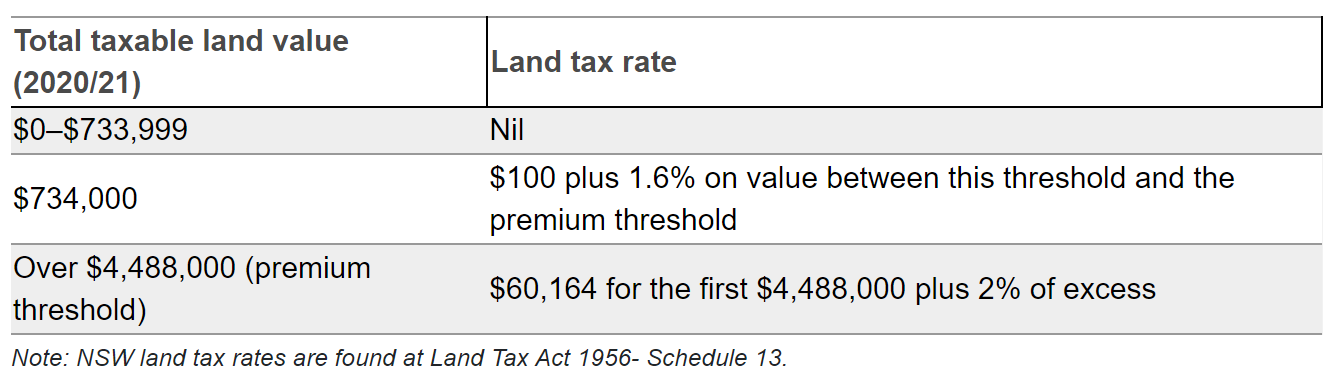

The rules and rates of land tax vary in each State or Territory. In NSW land tax is based on the value of land only (not buildings) and is calculated on a calendar year.

If the property is used as the home of the owner and/or their spouse, land tax generally does not apply. Other exceptions may also apply.

NSW land tax

Land tax is applied for the full year following the taxing date of 31 December, and no pro-rata calculation applies.

Exemptions/concessions

Land tax may not apply on the former home for up to six years after moving out of the home, provided the client had lived there for at least six months and does not move into another home that they own, for example they move into residential aged care. To receive this exemption the home must not be rented out for more than 6 months in a calendar year.

Exemptions may apply on land used for primary production.

If the property was the principal place of residence of a deceased person, it may be exempt from land tax for up to two years after the date of death or until the ownership is transferred.

If a person has a life interest from a deceased estate to occupy a home, that home may be exempt from land tax. The same applies if a person who had been living with the owner (before his/her death) is given permission by the executor to continue living in the home.

Note: exemptions may not apply if the home is owned by a company or trust.

Warning: This information provides a quick summary of land tax implications for a client moving into residential aged care in NSW. It does not cover all rules or exemptions for land tax.

You should not rely on this information as a comprehensive summary of land tax rules. For further details on Land Tax go to the Land Titles office in the relevant state to determine the implications for land tax.

When making important financial decisions regarding aged care, it is important to consider seeking independent financial advice to explore all the options available and understand the costs and impact of each option.

Find out more

Sophie is a Financial Aged Care Specialist at Morgans Gosford and is passionate about helping families answer questions like " do we have to sell the family home, what are the fees, how do we complete all the paperwork? " Sophie works through all these questions, plus many more. She creates financial strategies tailored to meet your loved ones goals and objectives, including covering their ongoing care needs. Sophie provides families with options and peace of mind.

If you would like to discuss getting financial aged care advice for yourself, or a loved one, please contact Sophie on [email protected] or via (02) 4325 0884 General Advice warning: This article is made without consideration of any specific client’s investment objectives, financial situation or needs. It is recommended that any persons who wish to act upon this report consult with their investment adviser

General Advice warning: This article is made without consideration of any specific client’s investment objectives, financial situation or needs. It is recommended that any persons who wish to act upon this report consult with their investment adviser before doing so. Morgans does not accept any liability for the results of any actions taken or not taken on the basis of information in this report, or for any negligent misstatements, errors or omissions.