Yesterday, the Reserve Bank of Australia (RBA) board met and reduced the Australian cash rate by 25 basis points to 4.1%. At the same time, they released the Quarterly Statement of Monetary Policy, which provides a broad range of outlooks for various variables affecting the Australian economy. The release of this report, on a quarterly basis alongside the RBA meeting, serves a similar function to the Summary of Economic Projections released by the Federal Reserve.

The RBA’s initial message was that even with the reduction in monetary policy, the outlook remains restrictive. However, according to our own model, A Cash Rate of 4.1% is not restrictive, but modestly expansive. Our model is based on 35 years of data.

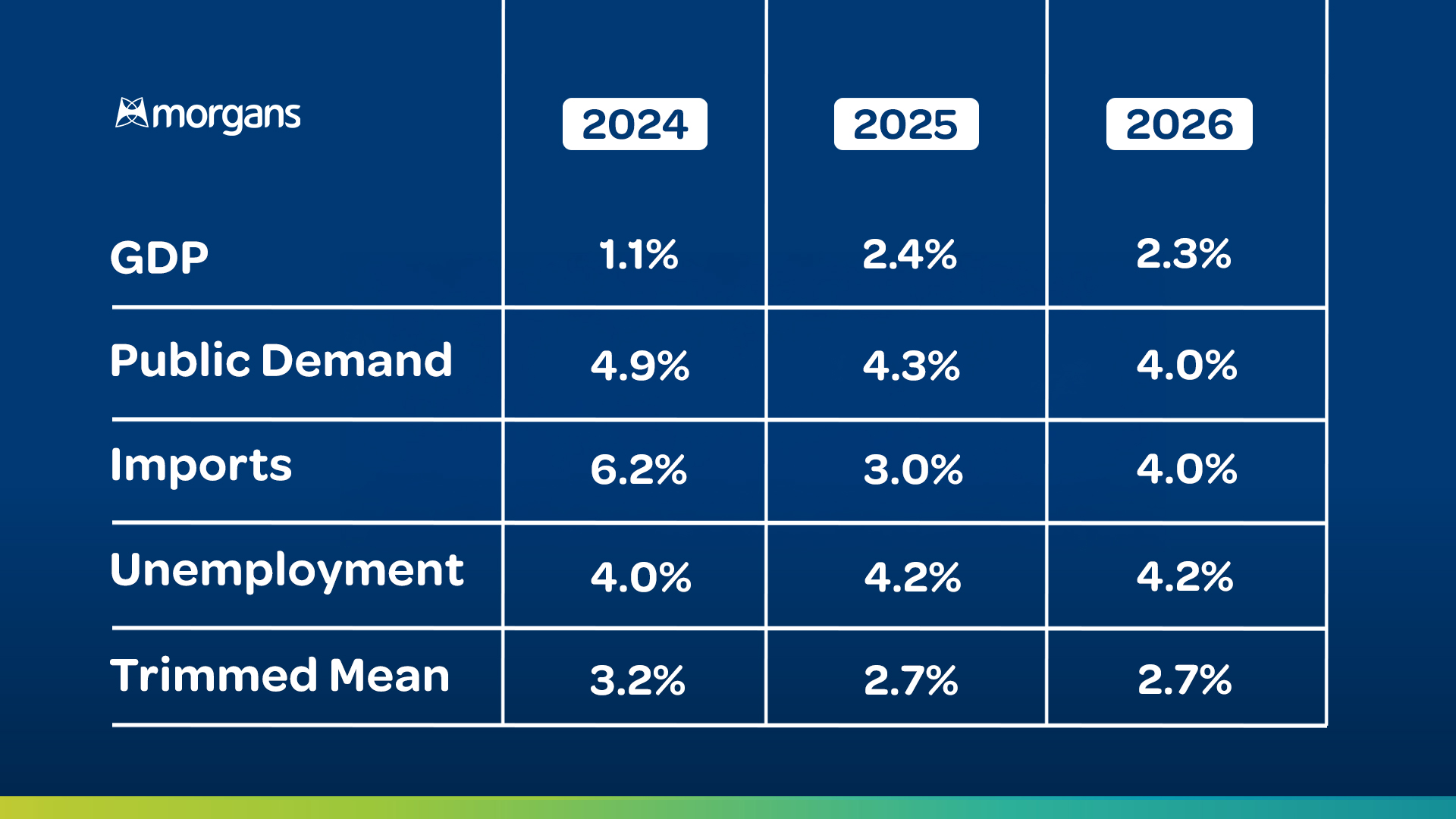

The Quarterly Statement indicated that the outlook for the Australian economy is for considerable expansion. After last year’s GDP growth of only 1.1%, which economists consider a soft landing, growth is projected to pick up, with a forecast of 2% for the year to June 2025. This is followed by 2.4% for the year to December 2025 Growth continues between 2.3% and 2.5% over the following years. Even in 2027, growth is expected to remain above 2%. This represents a promising future for the Australian economy. Interestingly, business investment is not expected to be the main driver of this growth. Business investment growth for the year to December was zero and is expected to remain at zero for the year to June, only growing by 1.4% by the end of 2025. It seems that growth will accelerate only after the economy picks up speed. Household consumption is also forecast to increase slightly from 0.7% last year to 2.6% this year.

The primary factor driving the anticipated growth is Public Demand, largely funded by "other people’s money". Public Demand (Government Spending) grew by 4.9% in the year to December 2024 and is expected to grow by 5.3% or more for the year to June 2025, with projections of 4.3% for December 2025 and 4% for 2026. This growth in public demand, largely financed through public borrowing, includes Federal and State Government spending, particularly on infrastructure projects. While this expansion will stimulate demand, it will be paid for later by taxpayers.

The unemployment rate, currently at 4%, is expected to rise slightly to 4.2% mid-year, where it is anticipated to remain. The RBA has indicated that this increase in unemployment will help reduce inflation, although not to the target of 2.5%. Inflation is projected to fall from a trimmed mean of 3.2% for the year to December 2024, to 2.7% by June 2025. However, inflation is expected to stabilise at this level, not reaching the 2.5% target.

This raises an interesting question: why does the RBA believe that inflation can fall to the lower end of the 2-3% range without unemployment reaching 4.6-4.7%, as suggested by historical data? We believe that the significant import boom in Australia, with imports rising by 6.2% for the year to December 2024, has played a role. Import growth is expected to slow in the coming years. We think that but year's surge in imported manufactured goods at low prices has created an illusion of sustainable low inflation at the same time as relatively low unemployment.

Our analysis suggests that such low inflation is unsustainable unless unemployment rises to 4.6% or higher. This issue may resurface in the coming quarters as the true challenges of reducing inflation are revealed. However, for now, we can say that the Australian economy appears to have bottomed out. We’ve had our soft landing with 1.1% growth in December 2024, and growth is now accelerating, even if it is being driven by public spending. By the end of 2025, growth is expected to reach 2.4%, and the economy is set to maintain above 2% growth for the next several years. This represents a strong recovery, and the Australian economy appears poised for a period of better performance in the coming years.

Morgans clients receive access to detailed market analysis and insights, provided by our award-winning research team. Begin your journey with Morgans today to view the exclusive coverage.