Staking it all on tax cuts and cost-of-living relief

The government largely pre-announced the 2025-26 Federal Budget over the past week. Handing down a deficit in 2024-25 and delivering further cost-of-living relief. The government did keep a tax cut up its sleeve and announced a reduction in the tax rate for all taxpayers. While there's a little bit for everyone, the forecast deficits for the next four years limit the government's ability to push harder on spending. Still, there's no denying this is a pre-election budget designed to appeal to the mainstream voter by putting spending ahead of saving.

Treasurer Jim Chalmers' fourth Budget shows the government is on track to achieve a budget deficit of $27.6bn, a slight deterioration from MYEFO that predicted a $26.9bn deficit. A range of upside surprises again drove revenue (the strong labour market, strong wage growth, and net overseas migration) but was offset by higher-than-forecast spending.

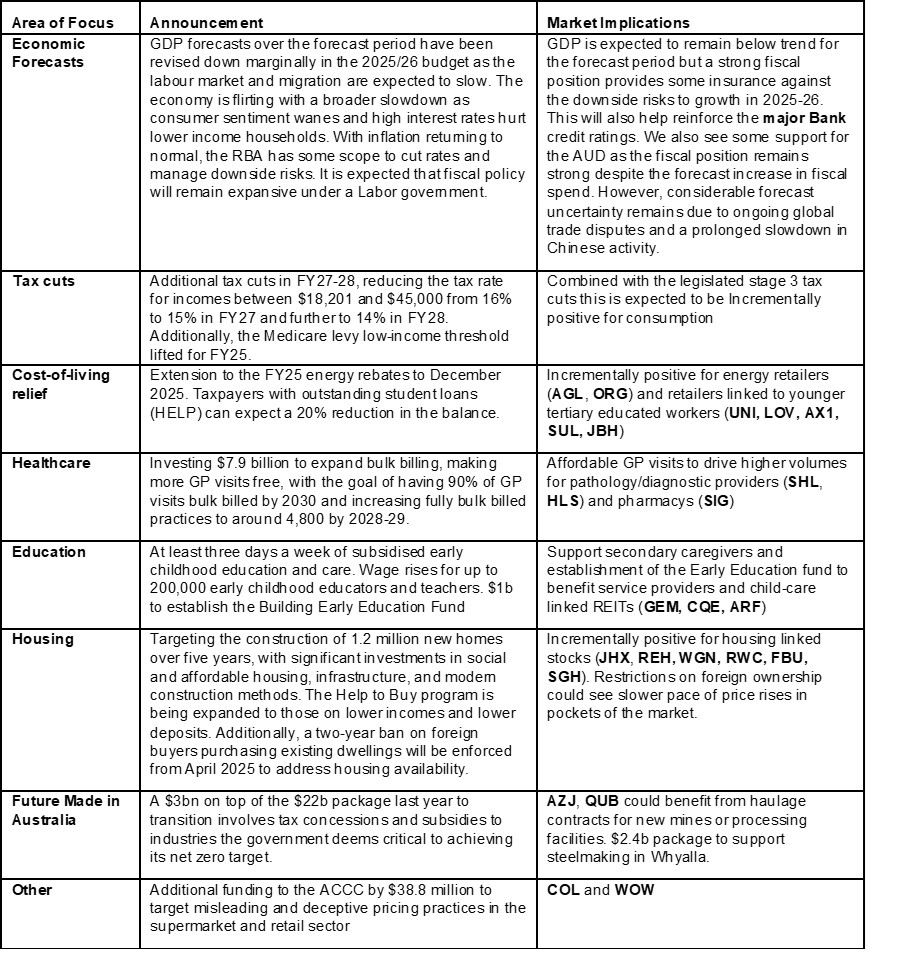

The key announcements were tax cuts, the extension of the energy rebates, GP bulk-billing funding and further support for the "Future Made in Australia" program. However, there has been no meaningful attempt to tackle structural pressures from NDIS, aged care, and health care, which has seen growth outpace inflation over the past few years.

Ahead of the election, this was the last chance for the government to demonstrate their economic credentials. Without meaningful reform, a helping hand from commodity prices, and a strong labour market, this Budget was underwhelming from a market perspective. In summary, the measures announced today will unlikely move the dial on market sentiment.

And there goes the surplus – The Budget swings back into a deficit in FY25 (-1.0% of GDP), which is forecast to remain over the forecast period (FY26-FY29). Deficits are expected over forward estimates as commodity prices ease and unemployment set to rise. Also, extra spending commitments (tax cuts, changes to Medicare and changes to education) will weaken the fiscal position over the forecast period. The capacity for the economy to absorb higher interest repayments will be tested over the next few years if government revenue declines as economic conditions deteriorate as expected.

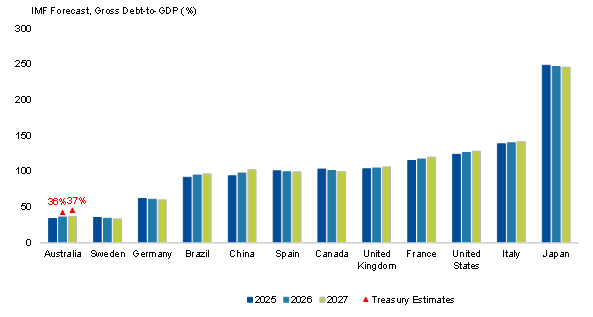

Treasury's forecast for gross debt rises from A$940b in 2024-25 (33.7% of GDP) to peak at A$1,161b in 2027-28 (36.9% of GDP). However, Australia's fiscal position remains well below peers global peers, which reinforces the highest possible sovereign credit rating.

World Gross Debt-to-GDP (IMF Forecasts and Treasury Estimates)

• Mildly inflationary but no big deal for equity markets – taking everything into account, a surprise tax cut, a bump in government spending, and some targeted measures to address cost-of-living pressure should not worry investors. Importantly for the market, a strong fiscal position and few inflation-inducing spending measures should also reassure investors that a slowdown is possible without a recession.

• A few more consumption levers were pulled this year ahead of the election – As anticipated, an extension to the energy rebates and changes bulk-billing and Medicare were announced. The government also surprised us by announcing a tax cut for all taxpayers, with the average worker expected to save $268 in FY27 and $536 in FY28. It also announced support for students with outstanding HELP debt by reducing the balance by 20%. All considered, the measures incrementally support consumption and sentiment.

• Budget assumptions and a cut expected to net overseas migration – Forecasts provide a low hurdle for the December MYEFO and next year's Budget. Key commodities are assumed to decline from elevated levels with iron ore price assumed to decline from US$101/tonne to US$60/tonne by March 2026; the metallurgical coal spot price declines from US$188 to US$140/tonne; the thermal coal spot price declines from US$97 to US$70/tonne. The AUD is expected to remain at 62c through the forecast period. The Budget expects net overseas migration to be 335,000 this year, after 435,000 last year. The government forecasts that it will fall to 260,000 in FY26, to 225,000 in the following years. Notably the RBA cash rate is assumed to fall a further 50bps in 2025.

Our thoughts

The quest for re-election is staked on the success of this Budget. Labor's fourth attempt put aside fiscal restraint and delivered a suite of spending promises. It was clearly designed to appeal to the mainstream voter by putting tax cuts front and centre promising something for every taxpayer. Changes to Medicare and some cost-of-living relief will provide some support for domestic demand, which in our view is mildly inflationary but unlikely to move the dial meaningfully on corporate profitability.

Successive governments have lacked the determination to bring about significant structural reform, chiefly around genuine tax reform, productivity and housing. This Budget is no different. The lack of genuine long-term reform through a period when the federal balance sheet has been boosted by elevated tax revenues, a strong job market and higher than expected commodity revenue is a missed opportunity for Labor.

In our view, the Budget is unlikely to bring about significant revisions to corporate earnings, however the ongoing commitment to support the vulnerable parts of the economy should help market sentiment and support earnings confidence. We prefer a targeted portfolio approach favouring quality (strong cashflow and market position e.g. JHX, DBI, QBE, CSL), and select cyclicals (QAL, UNI, ALQ, ORI, BHP). See our Best Ideas for our most preferred exposures.

Morgans clients receive access to detailed market analysis and insights, provided by our award-winning research team. Begin your journey with Morgans today to view the exclusive coverage.