For much of the past several years, investors have been focused on inflation, interest rates, geopolitical conflicts and central bank policy. While these issues continue to influence short-term market movements, some of the most significant drivers of future investment returns are developing more quietly beneath the surface.

One of those structural forces is demographics.

Recent research from Goldman Sachs, Demographics to Demand (June 2026), argues that ageing populations and declining birth rates are no longer simply social or economic issues—they are becoming measurable drivers of corporate earnings, industry demand and long-term investment performance. Goldman Sachs' analysis suggests that these demographic shifts are already influencing company revenues today and are likely to become increasingly important over the remainder of this decade.

Importantly, Goldman Sachs is not alone in this view. BlackRock's Investment Perspectives: Mega Forces identifies demographic divergence as one of the defining structural themes reshaping global economies alongside artificial intelligence, geopolitical fragmentation and the transition to a low-carbon economy. Together, these independent research papers reinforce an important message for investors: the world's demographic profile is changing, and investment portfolios should be prepared accordingly.

Key Summaries

- Demographic investing trends are becoming one of the most important structural drivers of long-term investment returns.

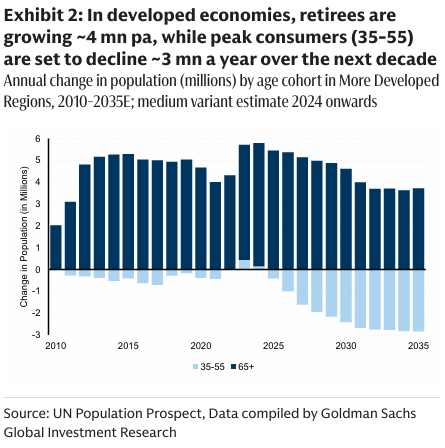

- Goldman Sachs estimates developed economies will add approximately four million retirees annually while the population of peak consumers aged 35–55 begins declining by around three million people each year from 2030.

- These population changes are already creating measurable tailwinds for some industries and headwinds for others.

- BlackRock identifies demographic divergence as one of the world's defining investment megatrends, reinforcing the long-term importance of this structural shift.

- Investors should increasingly focus on businesses positioned to benefit from enduring demographic demand rather than relying solely on short-term market cycles.

Demographics Are Becoming an Investment Variable

Population trends have traditionally been viewed through the lens of government policy, healthcaresystems or labour markets. Goldman Sachs argues that this perspective isbecoming outdated.

Their newly developed Demographic-Driven Demand (DDD) Framework examines approximately 3,000 listed companies globally by combining demographic forecasts, consumer spending behaviour across different age groups and geographic revenue exposure. The objective is to identify which companies and industries are likely to experience structural demand tailwinds or headwinds aspopulations continue to age.

The results are compelling.

Goldman Sachs estimates that industries with the strongest demographic tailwinds could experience anannual demand growth advantage of approximately 0.6 percentage points compared with industries facing the greatest demographic headwinds. More importantly forinvestors, companies with stronger demographic demand profiles have also generated larger revenue surprises and fewer earnings disappointments over thepast three years.

This suggests demographic positioning is no longer simply a long-termforecasting exercise—it is increasingly being reflected in current corporateperformance.

The World Is Ageing Faster Than Expected

The demographic story extends well beyond longer life expectancy.

Goldman Sachs highlights that rapidly declining fertility rates are accelerating population ageing across both developed and many emerging economies. While global population growth continues, its composition is changing dramatically.

By 2050, the global population aged over 65 is expected to double from approximately 800 million to 1.6 billion people. At the same time, many developed economies have already reached, or are approaching, peak populations within their traditional spending years of 35 to 55 years of age.

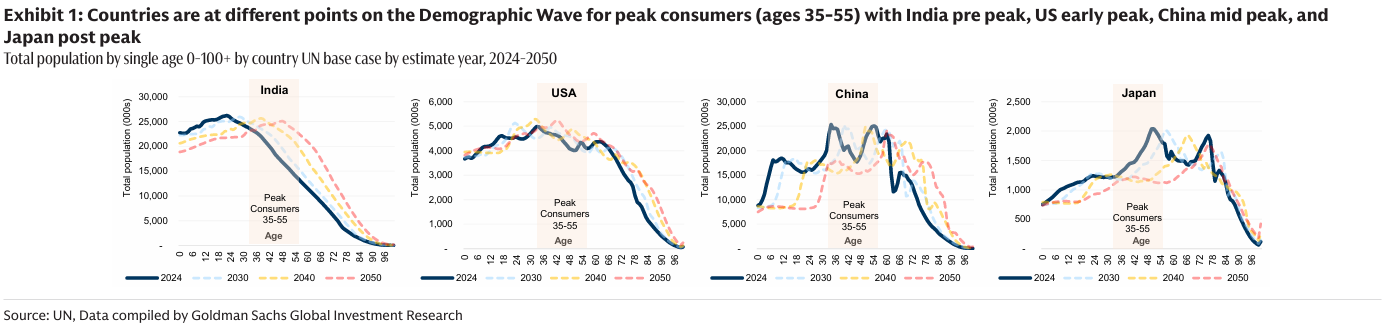

Different countries are progressing through this demographic transition at varying speeds. Goldman Sachs describes India as being in a "pre-peak" phase, the United States as "early peak", China as "mid-peak" and Japan as "post-peak". These differences have important implications for future economic growth, consumer demand and investment opportunities across regions.

Australia is comparatively well positioned among developed economies, benefiting from relatively stronger population growth and migration, although it is not immune to the broader ageing trend. Goldman Sachs identifies Australia as one of the countries expected to experience a relative improvement in its demographic profile compared with many other developed nations over coming decades.

Changing Populations Mean Changing Consumer Demand

One of the more interesting conclusions from Goldman Sachs' research is that demographic change influences not only the number of consumers but also what they buy.

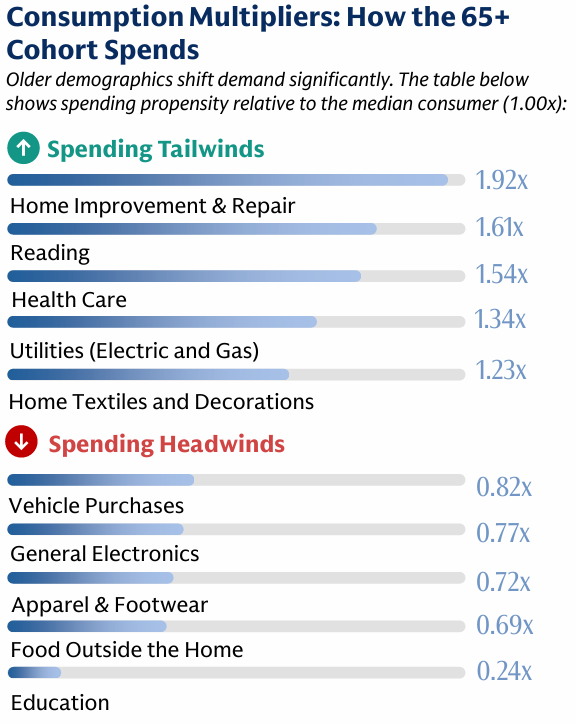

As consumers age, spending priorities naturally evolve. Analysis of spending data across the United States, Europe and Japan shows older households consistently allocate more of their expenditure towards healthcare, home maintenance, utilities and household furnishings. Conversely, spending on education, clothing, restaurants, consumer electronics and new vehicle purchases generally declines.

These changing consumption patterns create structural winners and losers across industries.

According to Goldman Sachs' framework, sectors expected to experience the strongest demographic tailwinds include:

Goldman Sachs estimates that the five industries with the strongest demographic tailwinds could experience demand growth of approximately 4.2% through 2030 and 8.7% through 2040, while industries facing demographic headwinds are expected to experience relatively weaker demand growth over the same period.

Naturally, demographics alone do not determine investment success. Innovation, competitive positioning, management execution and valuation remain critical considerations. However, demographic trends provide an increasingly valuable framework for understanding which sectors are likely to benefit from structural demand over many years rather than simply through the next economic cycle.

Independent Research Points to the Same Long-Term Trend

Perhaps the most compelling aspect of Goldman Sachs' findings is that they closely align with conclusions reached by BlackRock.

In its Mega Forces research, BlackRock identifies demographic divergence as one of the structural forces expected to reshape investment markets over the coming decades. Alongside advances in artificial intelligence, geopolitical fragmentation, digital infrastructure and the transition to cleaner energy, BlackRock argues that demographic changes will influence economic growth, inflation dynamics, labour markets and capital allocation.

While each organisation approaches the topic from a different perspective, both reach remarkably similar conclusions. Demographic change is not a distant possibility to monitor for future generations—it is already influencing corporate earnings, sector leadership and investment opportunities today.

Rather than viewing demographics as a standalone investment theme, investors should recognise that it interacts with many of today's dominant market narratives. Labour shortages are accelerating automation and artificial intelligence adoption. Ageing populations are driving increased healthcare demand. Rising electricity consumption associated with both ageing societies and digital infrastructure is supporting long-term investment in utilities and energy networks. These themes are increasingly interconnected rather than independent.

Positioning Portfolios for the Demographic Megatrend

One of the key lessons from both Goldman Sachs and BlackRock is that successful investing increasingly requires looking beyond the next quarter or even the next economic cycle. Structural themes, such as demographic change, unfold over decades and can create enduring opportunities for well-positioned businesses.

For investors, this does not necessarily mean building portfolios around a single theme or abandoning diversification. Instead, it reinforces the importance of owning high-quality businesses with sustainable competitive advantages that are aligned with long-term structural demand.

As populations age and labour markets tighten, companies that help improve productivity, automate repetitive tasks, provide essential healthcare services or support critical infrastructure may enjoy stronger and more resilient demand. Likewise, businesses operating in industries benefiting from recurring rather than discretionary spending may prove more resilient during periods of economic uncertainty.

Importantly, demographic trends also reinforce the value of global diversification. Countries are progressing through different stages of demographic transition, creating varying growth opportunities across regions. While Japan and much of Europe are experiencing advanced population ageing, economies such as India continue to benefit from younger populations and expanding workforces. Australia remains relatively well positioned compared with many developed nations due to stronger population growth and migration, although it too faces the longer-term challenges associated with an ageing society.

For long-term investors, understanding these regional differences can assist in identifying where future economic growth and corporate earnings are most likely to emerge.

What Investors Should Be Watching Now

Although demographic change is a multi-decade trend, its influence is already becoming evident across today's markets.

Many of the themes dominating financial headlines can be linked directly or indirectly to changing population dynamics.

These include:

- Ongoing labour shortages across developed economies.

- Increased investment in artificial intelligence and automation to improve productivity.

- Growing healthcare expenditure driven by ageing populations.

- Rising demand for electricity, utilities and digital infrastructure.

- Immigration policy debates aimed at supporting workforce participation.

- Increased government spending on healthcare, aged care and essential infrastructure.

Rather than viewing these as isolated developments, investors should recognise them as interconnected outcomes of a changing demographic landscape.

This perspective also provides important context during periods of market volatility. While interest rates, elections and geopolitical events can influence markets in the short term, structural demographic trends tend to evolve gradually and consistently, often providing clearer signals about where long-term earnings growth is likely to develop.

As always, however, demographics represent only one component of a robust investment process. Company fundamentals, valuation, balance sheet strength, management quality and broader economic conditions remain equally important considerations when constructing portfolios.

Conclusion

Markets will always be influenced by economic data releases, central bank decisions and geopolitical events. These factors remain important and deserve close attention. However, some of the most significant investment opportunities emerge from structural changes that unfold gradually over many years.

The convergence of research from both Goldman Sachs and BlackRock provides a compelling reminder that demographics are becoming one of those structural forces. Ageing populations, declining fertility rates and shifting patterns of consumer demand are already influencing industries, corporate earnings and capital allocation across global markets.

While no single investment theme should dictate portfolio construction, understanding these long-term trends can help investors position their portfolios to benefit from enduring sources of growth while remaining diversified across regions, sectors and asset classes.

As we continue to monitor economic conditions and market developments, demographic change is likely to remain an increasingly important consideration when assessing both risks and opportunities for long-term investors.

If you would like to discuss how these structural trends may influence your own investment strategy or portfolio positioning, please contact me for a personalised review.

Explore More Insights from Scott Fraser

This article is part of a broader collection of insights from Scott Fraser, covering a wide range of financial planning and investment topics.

Visit Scotts' page to read more articles, learn about their experience and approach, and choose whether you would like to connect with Scott via email or book in a meeting.

FAQs

What are demographic investing trends?

Demographic investing trends refer to investment opportunities created by long-term changes in population growth, ageing, birth rates and consumer behaviour. These trends can influence which industries experience sustained growth or face structural challenges over many years.

Why are demographics becoming more important for investors?

Population changes affect labour markets, consumer spending patterns and economic growth. As these changes become more pronounced, they increasingly influence company revenues, sector performance and long-term investment returns.

Which industries could benefit from ageing populations?

Research from Goldman Sachs suggests sectors including healthcare, pharmaceuticals, medical technology, insurance, utilities and consumer staples are well positioned to benefit from ageing populations and changing spending patterns.

Does this mean investors should avoid sectors facing demographic headwinds?

Not necessarily. Demographic trends are only one consideration when assessing investment opportunities. Innovation, global expansion, technological disruption and strong management teams can enable companies to outperform despite demographic challenges.

How does this relate to BlackRock's Megatrends research?

BlackRock identifies demographic divergence as one of several structural "Mega Forces" expected to reshape global markets alongside artificial intelligence, geopolitical fragmentation and the energy transition. Together with Goldman Sachs' research, this reinforces the importance of incorporating structural themes into long-term portfolio construction.

Disclaimer

This report was prepared by Scott Fraser through independent research facilities as a private communication to clients and was not intended for public circulation, publication or for the use of any third party, without the prior written approval of Scott Fraser. It does not constitute advice to any person. The views expressed here are those of the author and do not necessarily reflect those of Morgans Limited (ABN 49 010 669 726), its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”). Morgans may publish research on the company/s named here, which will be forwarded on request. While this report is based on information from sources which Scott Fraser considers reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Scott Fraser's judgement at this date and are subject to change. Morgans does not accept any liability for the results of any actions taken or not taken on the basis of information in this report, or for any negligent misstatements, errors or omissions. This report is made without consideration of any specific client’s investment objectives, financial situation or needs. It is recommended that any persons who wish to act upon this report consult with their investment adviser before doing so. This report does not constitute an offer, or invitation to purchase, any securities and should not be relied upon in connection with any contract or commitment whatsoever.