This article is a converted version of Michael Knox’s full presentation, which can be viewed in the video above.

Key takeaways

- Trimmed‑mean CPI rose to 3.4% in January 2026, sitting clearly above the RBA’s 2.5% midpoint target.

- Rising electricity prices are driving services inflation, with business pass‑through occurring 4–6 months after the initial increase.

- Inflation may peak later than expected, with our modelling pointing to December 2026 at around 4.4%.

- The RBA cash rate may also peak later and higher, potentially reaching 4.6% by November 2026.

Introduction

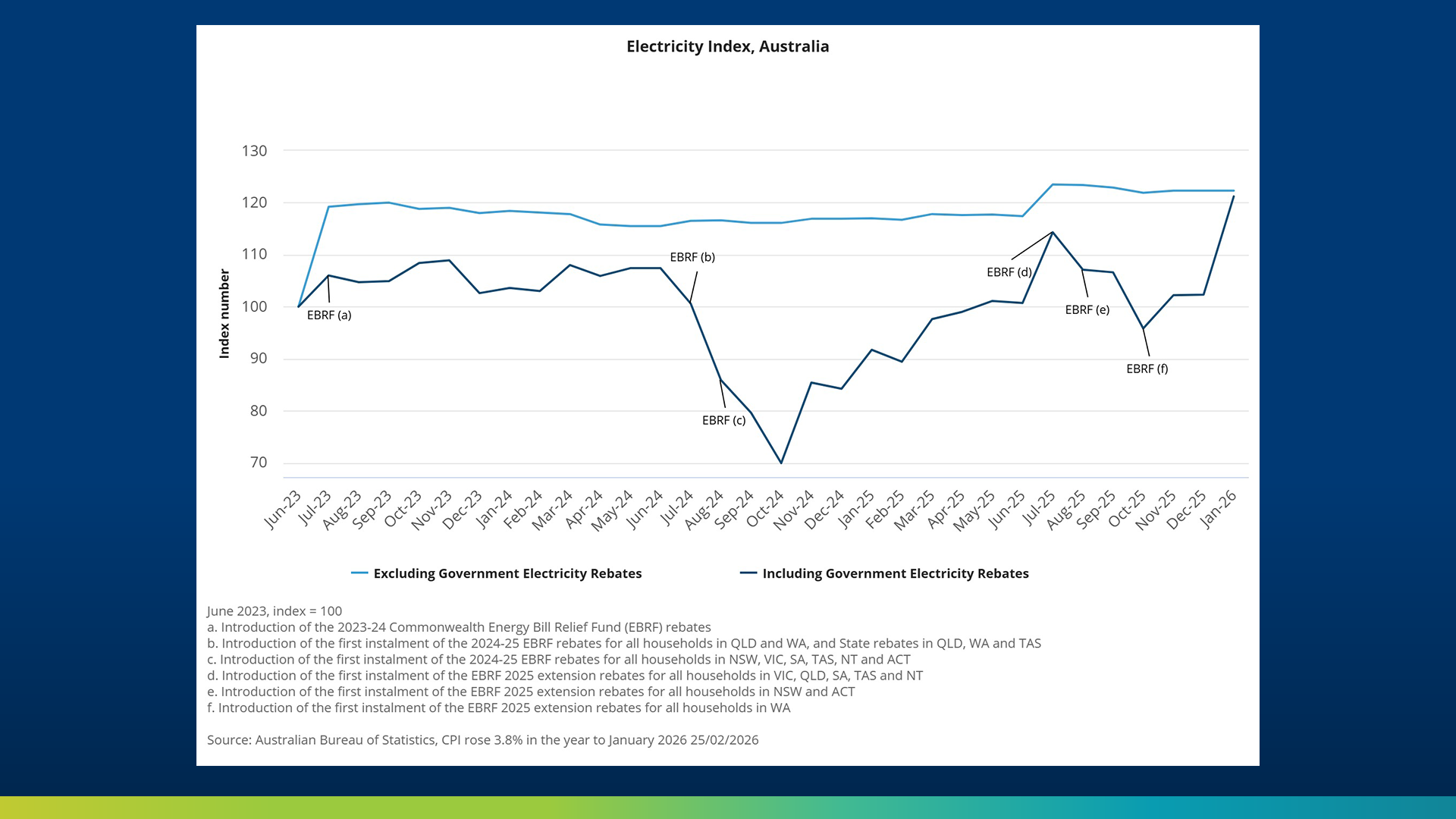

Australia’s inflation profile continues to shift as rising electricity prices place renewed pressure on services inflation. The trimmed‑mean CPI reading for January 2026 came in at 3.4%, noticeably above the RBA’s preferred midpoint of 2.5%.

While the common assumption is that electricity price increases are small and temporary, our analysis suggests they have a more powerful and delayed impact on overall inflation. Businesses face higher input costs immediately, but the true pass‑through to consumers occurs months later, creating what can be considered a second‑wave effect on CPI.

Why electricity matters more than expected

Government subsidies that previously kept electricity prices artificially low have now ended, resulting in retail prices rising toward actual generation costs. These increases lift operating expenses for both small and large businesses.

However, the key factor is timing. Firms rarely adjust prices overnight. Instead, electricity‑driven cost increases flow through gradually, typically 4 to 6 months after the initial price jump. As these higher costs filter through to the prices of goods and services, services inflation rises again, extending the overall inflation cycle.

This dynamic means the inflation pressures building now may be felt most acutely in the second half of 2026, not the first.

Expected timeline: a later inflation peak

Market consensus currently expects CPI to peak around 4.2% in June 2026. But when accounting for the delayed pass‑through of electricity prices, a different picture emerges.

Modelling suggests that Australia’s inflation peak is likely to occur later in the year, around December 2026, and at a higher level of 4.4%.

This later peak has important implications for households, investors, and policy expectations going into 2027.

Cash rate implications

A later inflation peak typically means a later cash‑rate peak. While market expectations point to a mid‑year peak around 4.2%, the modelling suggests the RBA may instead move towards 4.6% by year‑end, lifted by a sequence of rate increases spread across 2026.

Projected cash‑rate path for 2026

This sequence indicates one more rate hike in the first half of 2026, alongside one early‑year move already completed. Then, two more rate hikes in the second half of 2026.

What this means for businesses and households

1. Services pricing will remain firm

As electricity‑driven cost increases continue flowing through supply chains, services providers should lift prices again in the second half of 2026.

2. Energy budgeting becomes critical

With subsidies removed, higher electricity bills for households and businesses should be expected throughout the year.

3. Borrowing costs may stay elevated longer

If the cash rate peaks later, refinancing and major financing decisions may be better timed for 2027 rather than late 2026.

FAQs

Why is electricity influencing inflation so strongly?

Electricity is a core cost across nearly every sector. When prices rise, businesses eventually pass these higher costs on to consumers after a 4–6 month delay.

When is inflation likely to peak?

Modelling points to a December 2026 peak instead of mid‑year, due to delayed pass‑through from electricity to services inflation.

How many rate hikes are still expected?

Three more increases are likely, with two in the second half of the year, potentially lifting the cash rate to 4.6%.

Is this a temporary inflation burst?

Not entirely. While electricity is the immediate driver, the lagged effects across services suggest the impact will extend well into late 2026.

Conclusion

Electricity prices are becoming a defining factor in Australia’s 2026 inflation story. With subsidies withdrawn, rising energy costs are working their way through the economy more slowly but more forcefully than commonly assumed.

This delayed pass‑through means both inflation and the cash rate may peak later in the year than consensus expects. For households, businesses and investors, planning for a later and slightly higher peak will be essential.

Want to discuss how this impacts your portfolio?

DISCLAIMER: Information is of a general nature only. Before making any financial decisions, you should consult with an experienced professional to obtain advice specific to your circumstances.