Today’s focus is on the sharp increase in Australian CPI and what it means for the trajectory of monetary policy for the Reserve Bank of Australia . Headline CPI rose by 4.6 per cent for the year to March, a significant jump from 3.7 per cent in February. However, the RBA does not base its decisions on headline inflation. Instead, it focuses on core inflation, measured by the trimmed mean, which remained unchanged at 3.3 per cent in both February and March. This remains well above the RBA’s target of 2.5 per cent, suggesting that interest rates will continue to rise until core inflation returns to target.

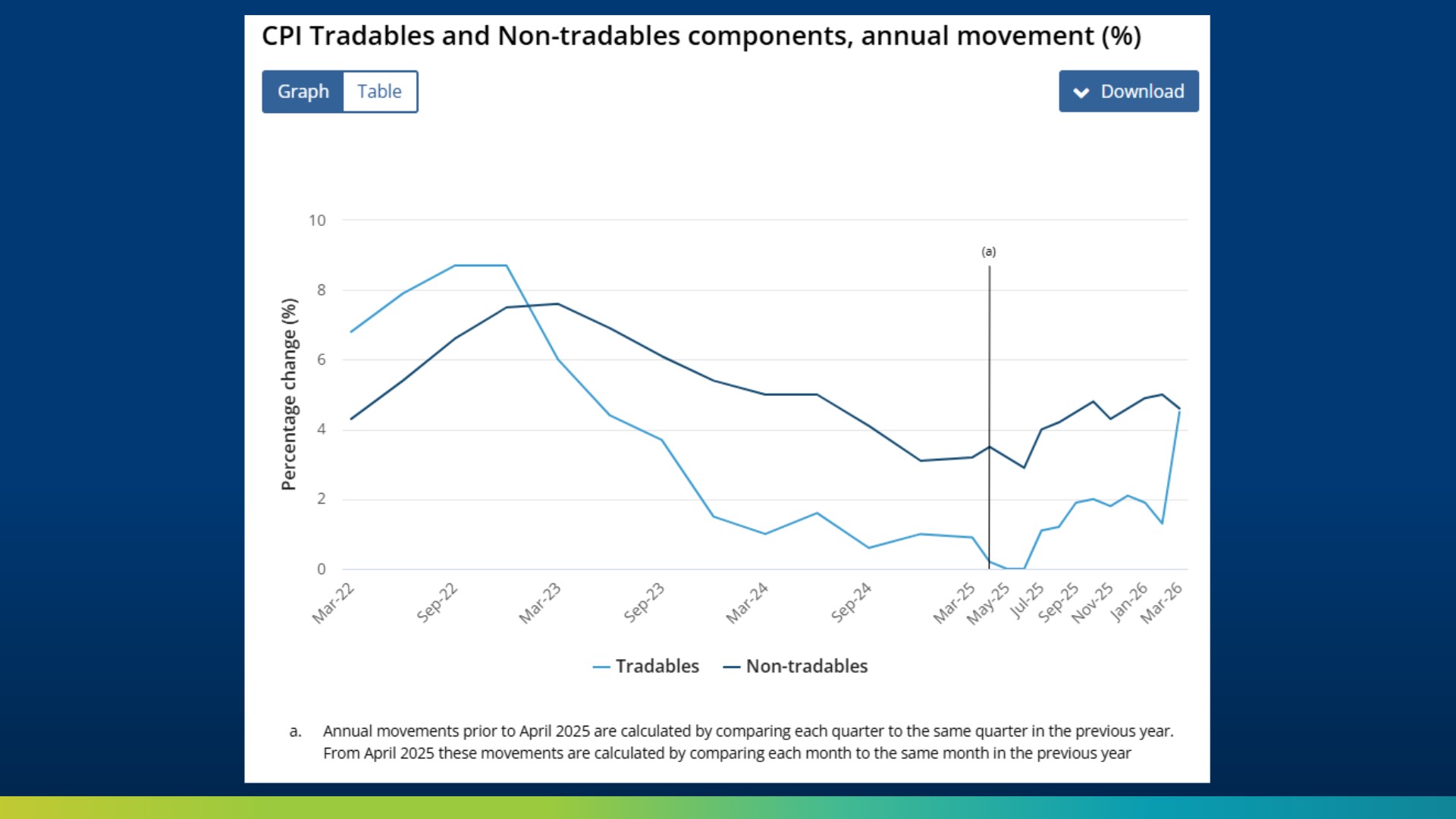

A key driver of inflation outcomes since early 2022 has been the divergence between private sector and public sector inflation, as shown in CPI tradable and non-tradable components. Tradable components broadly reflect private sector activity, while non-tradable components largely align with the public sector, including essential services such as electricity. The data from March 2022 onwards, coinciding closely with the commencement of the Albanese government, provides a clear picture of how inflation pressures have evolved during this period.

Initially, private sector inflation was higher, driven by a commodities boom. In response, the RBA lifted interest rates aggressively. These rate hikes proved extremely effective in reducing private sector inflation, with tradable goods inflation falling from over 8 per cent in September 2022 to around zero by March to May 2025. By contrast, public sector inflation proved far more persistent, declining from just under 8 per cent in late 2022 to only just under 4 per cent by 2025. A major factor behind this persistence has been rising electricity costs.

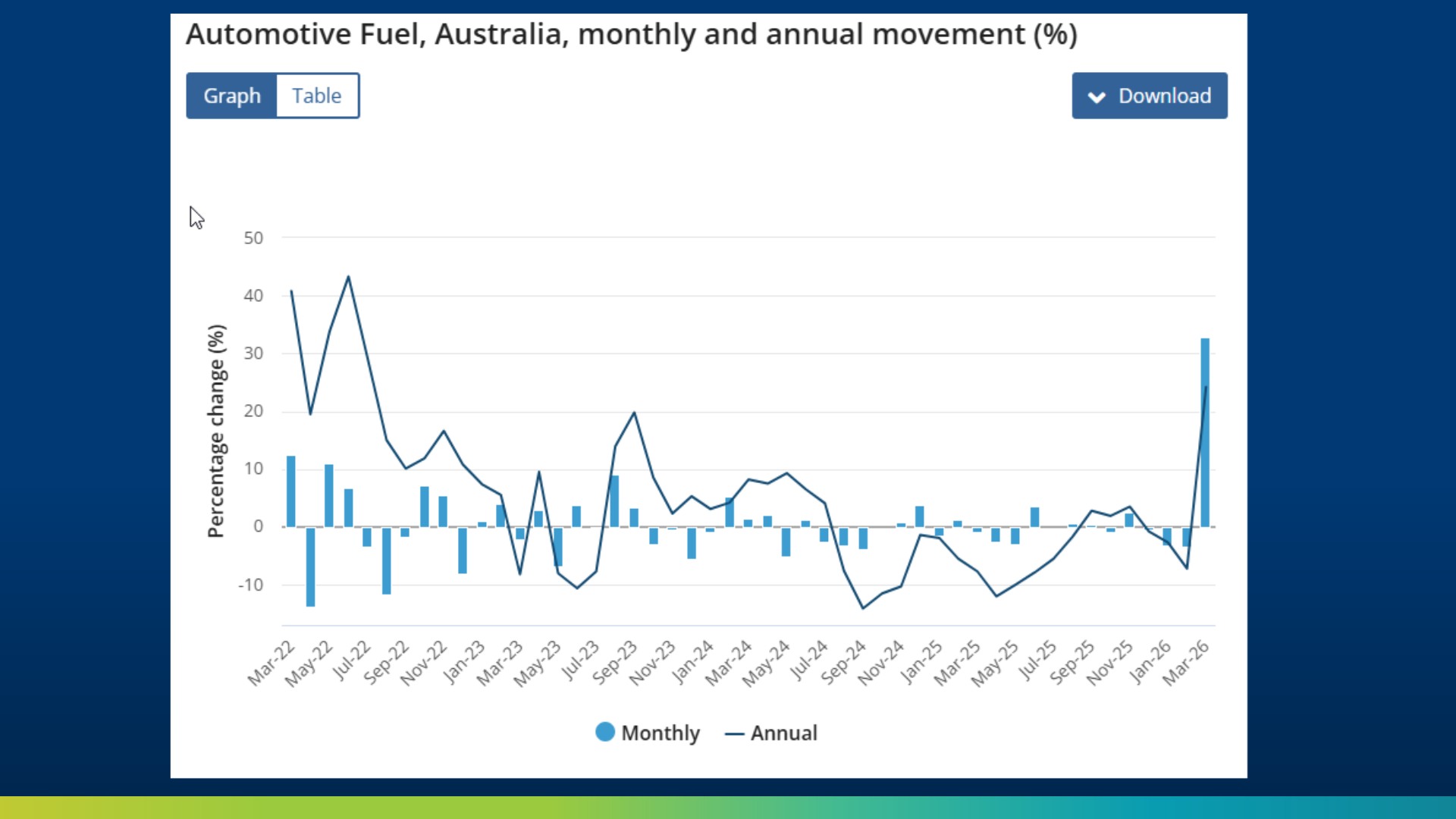

By February this year, the difference between public and private sector inflation was stark. Public sector inflation was running at 5.6 per cent, while private sector inflation had fallen to just 1.3 per cent. This clearly shows that the private sector was doing almost all of the work in driving inflation lower across the economy. However, in a single month, rising oil and petrol prices caused private sector inflation to surge from 1.3 per cent to 4.5 per cent, lifting it temporarily to levels closer to public sector inflation.

This pattern reflects a period of private sector recession alongside a public sector boom. Public spending growth and elevated costs in government-influenced services have kept overall inflation high, despite significant weakness and adjustment in private sector pricing.

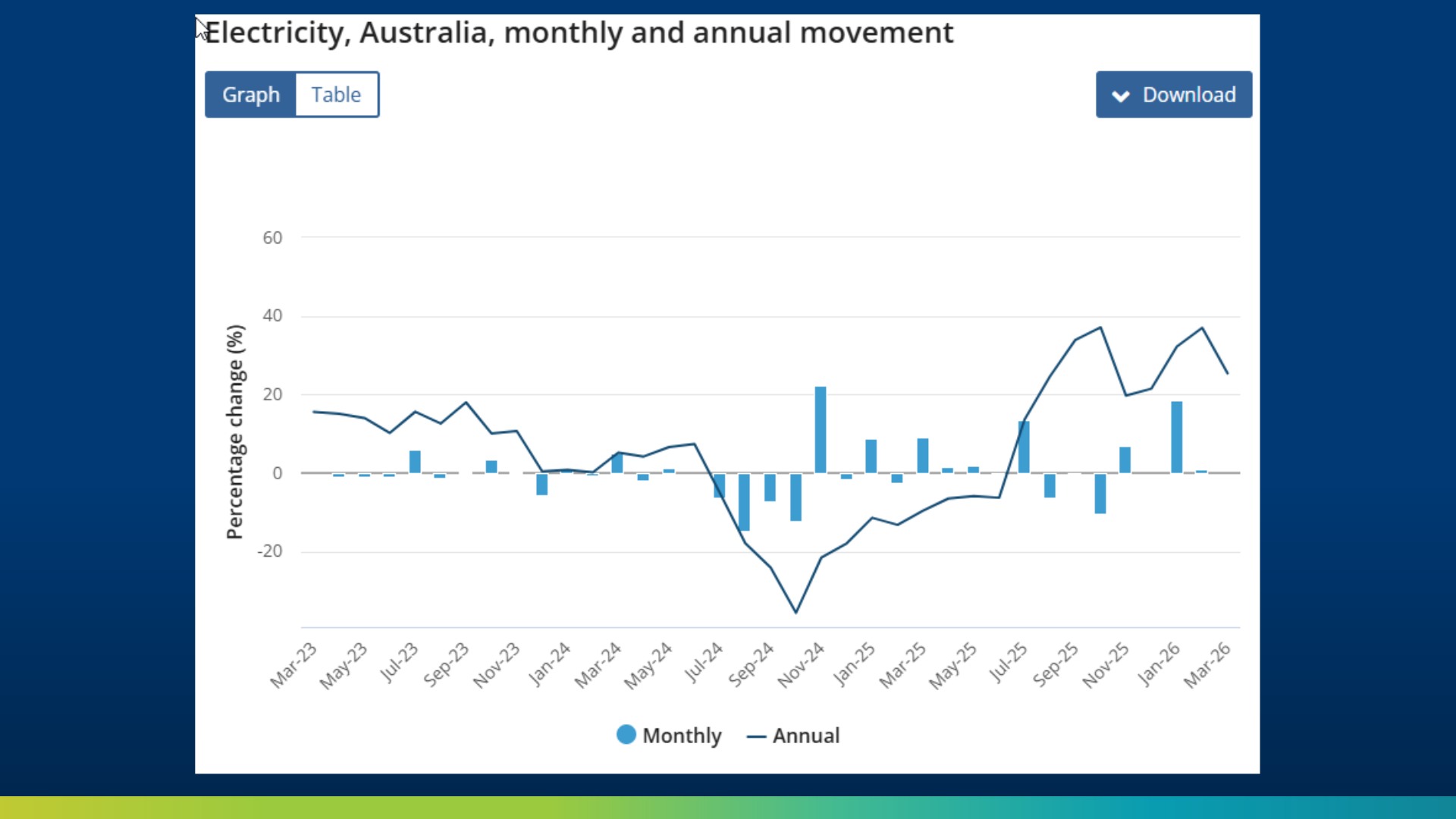

Electricity prices provide a clear example. In 2024, substantial government subsidies of around $9 billion per year kept retail electricity prices low, pushing annual price changes into negative territory as late as November 2024. However, following the election in the first half of 2025 and the winding back of subsidies, electricity prices accelerated sharply. Annual electricity price growth swung from -6.3 per cent in June 2025 to +37.1 per cent by October 2025. Even by year-end, annual electricity prices were still rising at over 21 per cent, reaching 25.4 per cent for the year to March.

At the same time, the recent acceleration in petrol prices pushed tradable goods inflation higher in March, largely driven by geopolitical tensions, including the conflict involving Iran. Automotive fuel, which had previously been subtracting from inflation as recently as February, suddenly became the dominant contributor. In March alone, fuel accounted for 0.8 percentage points of the total 4.6 per cent CPI outcome.

Looking ahead, the implications for monetary policy are clear. While headline inflation has risen, core inflation remains unchanged at 3.3 per cent, still well above the RBA’s target. Our Australian Cash Rate model suggest the Australian cash rate will need to rise to an equilibrium level of around 4.95 per cent, significantly higher than the current cash rate of 4.1 per cent.

As a result, it is expected that the RBA will raise rates at its upcoming meeting, with further increases likely over the course of the year.

Want to discuss how this impacts your portfolio?

DISCLAIMER: Information is of a general nature only. Before making any financial decisions, you should consult with an experienced professional to obtain advice specific to your circumstances.