I want to discuss a simplified explanation of the US business cycle, prompted by the International Monetary Fund's forecast released yesterday, which, for the first time, assessed the impact of tariffs on the US economy. Unlike last year's 2.8% growth, the IMF predicts a drop to 1.8% in 2025. This is slightly below my forecast of 1.9 to 2%. They further anticipate growth will decline to 1.7% in 2026, lower than my previous estimate of 2%. Growth then returns to 2% by 2027.

This suggests that increased tariffs will soften demand, but the mechanism is intriguing. Tariffs are expected to reduce the US budget deficit from about 7% of GDP to around 5%, stabilizing government debt, though more spending cuts are needed. This reduction in US deficit reduces US GDP growth. This leads to a slow down.

The revenue from tariffs is clearly beneficial for the US budget deficit, but the outlook for the US economy now points to an extended soft landing. This is the best environment for equities and commodities over a two-year view. With below-trend growth this year and even softer growth next year, interest rates are expected to fall, leading the fed funds rate to drift downward in response to slower growth trends. Additionally, the US dollar is likely to weaken as the Fed funds rate declines, following a traditional US trade cycle model: falling interest rates lead to a weaker currency, which in turn boosts commodity prices.

This is particularly significant because the US is a major exporter of agricultural commodities, has rebuilt its oil industry, and is exporting LNG gas. The rising value of these commodities stimulates the economy, boosting corporate profits and setting the stage for the next surge in growth in a couple of years.

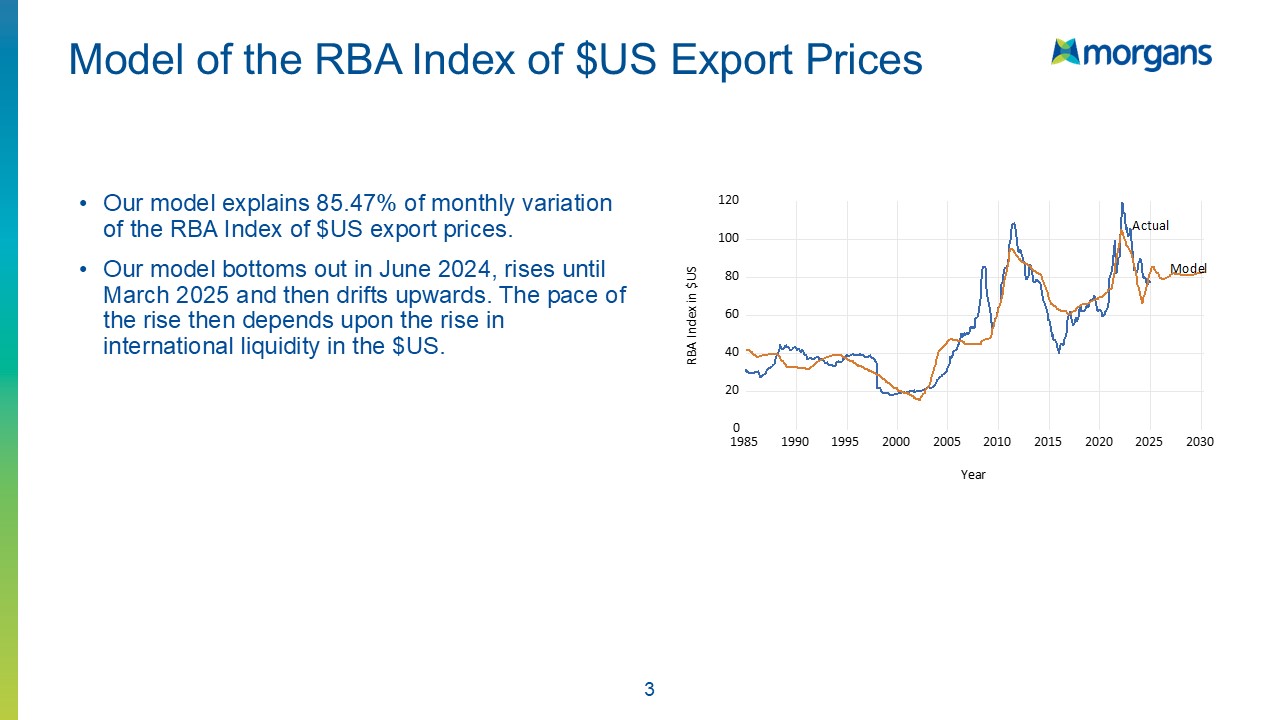

This outlook includes weakening US interest rates and rising commodity prices, continuing through the end of next year. This will be combined with corporate tax cuts, likely to be passed in a major bill in July, reducing US corporate taxes from 21% to 15%. This outlook is very positive for both commodities and equities. Our model of commodity prices shows an upward movement, driven by an increase in international liquidity within the international monetary system.

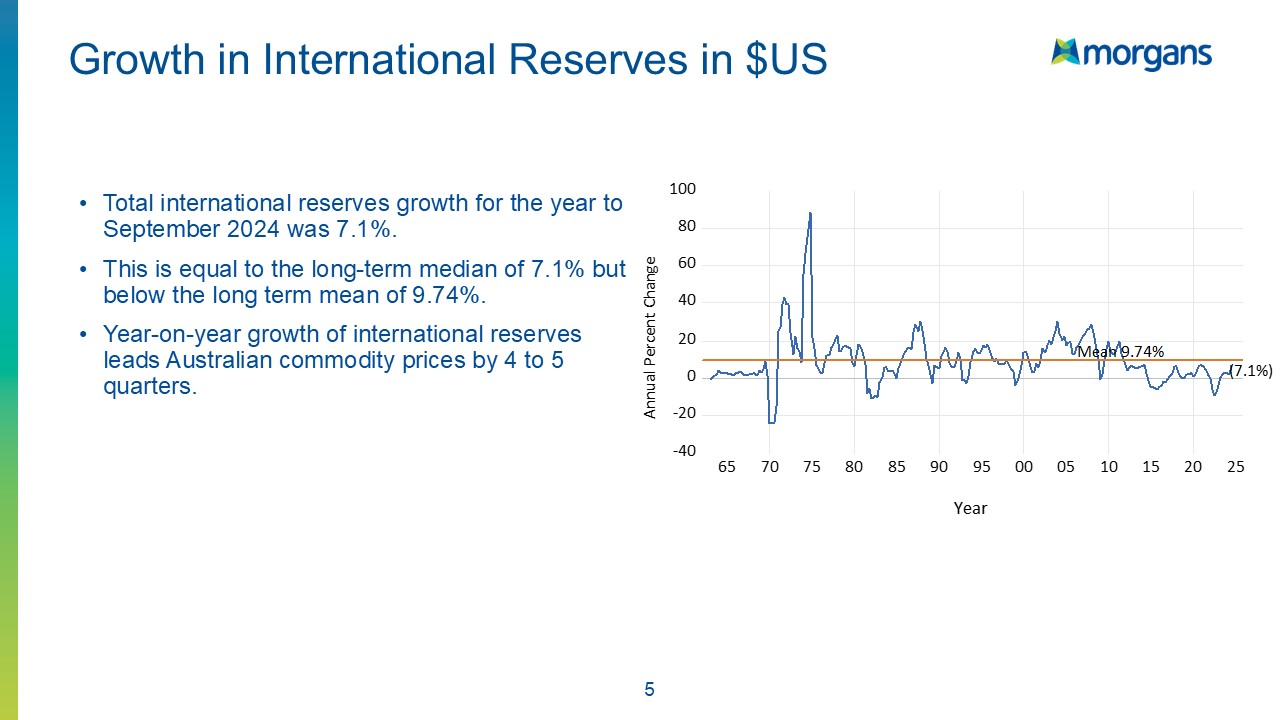

With US dollar debt as the largest component in International reserves , as US interest rates fall, the creation of US government debt accelerates, increasing demand for commodities. The recent down cycle in commodities is now transitioning to an extended upcycle through 2026 and 2027, fueled by this increased liquidity due to weaker interest rates.

Furthermore, the rate of growth in international reserves is accelerating, having reached a long-term average of about 7% and soon expected to rise to around 9%. Remarkably, the tariffs are generating a weaker US dollar, which drives the upward movement in commodity prices. This improvement in commodity prices is expected to last for at least the next two years, and potentially up to four years.