Key Takeaways

- Historical Performance: Shares have historically outperformed most other asset classes over the long term, particularly when including franking credits and dividend reinvestment.

- Leverage Advantage: Direct property allows for significant gearing, enabling investors to gain exposure to a large asset with a relatively small initial deposit.

- Liquidity & Accessibility: Shares offer high liquidity and low entry costs, whereas property is a tangible, "brick and mortar" asset with significant entry and exit hurdles.

- Tax Efficiency: Dividend imputation provides unique tax offsets for share investors, while property offers benefits through depreciation and negative gearing.

- 2026 Market Outlook: Property markets in cities like Perth and Brisbane show strong momentum due to supply shortages, while the ASX 200 remains a robust engine for compounding wealth.

Many investors swear by share investing. Others prefer the tangible security of direct property. What is best for you? The answer depends on your personal investment needs, your stage of life, and importantly, which strategy you are comfortable with. In 2026, with shifting interest rates and evolving tax regulations, the choice between these two powerhouses requires more nuance than ever before.

Investing in Shares: The Compounding Engine

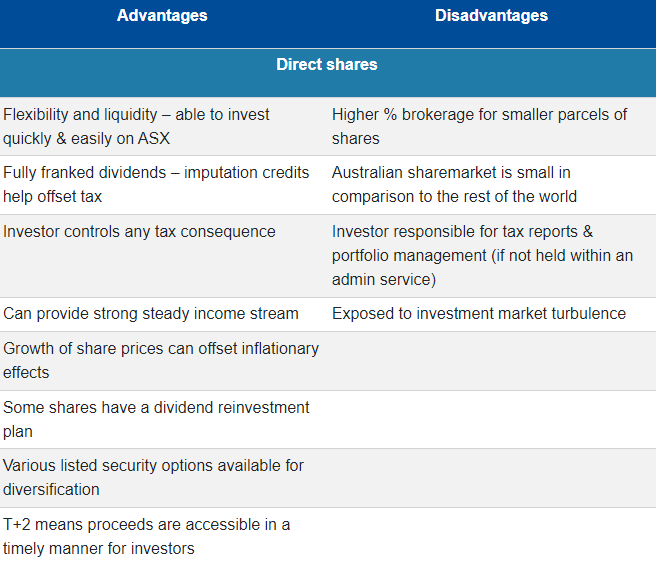

Shares have historically outperformed all other asset classes over the long term. Beyond the potential for capital growth, they provide a strong and growing income stream through dividends. For those looking for wealth management solutions that don't require managing tenants or maintenance, the share market is an efficient vehicle.

Why are Shares So Popular?

Investors are drawn to the share market for several reasons:

- Capital Growth: Direct shares offer the possibility that their price will rise over time, offsetting the effects of inflation.

- Dividend Reinvestment: Reinvesting dividends can multiply the compounding effect, significantly increasing your total return over 10 or 20 years.

- Liquidity: You can sell a parcel of shares in minutes. You cannot sell the back bedroom of an investment property if you need fast access to cash.

What are the challenges?

One of the more obvious challenges when investing in any sharemarket is volatility.

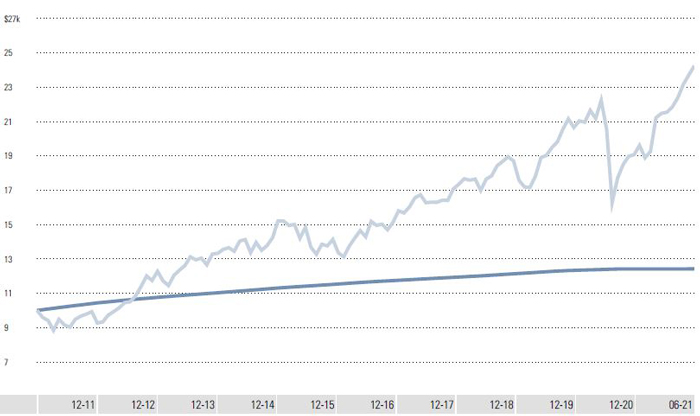

From the 'Black Monday' crash in 1987 to interest rates rising to around 18% in the late 80’s and early 90’s through to the general market decline in 1994, onto the 1997 Asian crisis and then the tech and internet stock boom and bust in 2000. Of course, we will never forget the 'GFC', or Global Financial Crisis, in 2008 and now, most recently, the significant fall and subsequent rise of markets through 2020 due to COVID-19.

Shares are often considered risky due to potential short-term performance volatility. Over the long term, however, shares have provided consistent investment returns.

Chart 1: Australian Shares (S&P/ASX200) vs Cash (Bloomberg AusBond Bank Bill Rate): 2011 to 2021

The Australian sharemarket is dominated by large institutions e.g. the banks, CSL and BHP. The financial sector makes up approx. 45% of the S&P/ASX200 Index. The performance of this sector, therefore, can influence the direction of the market.

Individuals invest in direct shares because they offer the possibility that their price will rise over time. Owning a share with a rising value provides growth from that investment - and an obvious benefit of capital growth is that it can offset the effects of inflation. In addition to rising share prices, dividends and dividend re-investment plans can multiply the capital growth effect of a share investment.

Note: Important disclosures can be found in the Disclosure Appendix

Tax Benefits via Franking Credits

The Australian imputation system remains a cornerstone of domestic share investing. Most companies listed on the ASX pay dividends that include franking credits (or imputation credits). This system prevents double taxation by allowing you to use the tax already paid by the company to offset your own income tax.

For example, a 4% fully franked dividend yield actually provides a "grossed-up" return closer to 5.7% for most taxpayers. This makes shares a highly attractive option for retirees or those in a Self-Managed Super Fund (SMSF), where excess credits can even be refunded as cash.

The imputation credit and resulting tax benefit available from the dividends means the actual return from that particular stock needs to be "grossed up" to reflect its true value. A common mistake investors make is comparing bank rates with dividend yields. The cash rate is fully assessable whereas the dividend yield includes the imputation credits, so you need to take this tax concession into account. For example, a 2.5% fully franked dividend yield is actually providing a grossed-up return of approximately 3.6% when you take into account the added tax benefit.

Table 2 highlights the grossed-up effect of various dividend yields, as well as the equivalent after tax yield based on flat 15% (super), 32.5% and 45% tax rates.

Table 2: Grossed-up effect of yield

Surplus Franking Credits

Where there is a surplus of franking credits due to the fact the individual or entity's tax rate is lower than the 30% company tax rate, the surplus credits are refunded to that individual or entity. For example, the maximum tax rate within superannuation is 15%. Fully franked shares within a self managed super fund (SMSF), therefore, provide a 15% tax credit. This credit can be used to offset tax on other income within the fund.

If the SMSF is in pension phase, where the tax rate is 0%, franking credits are fully refunded back to the fund. This has the effect of 'topping up' the pension's account balance. Over time this can add substantial value to the fund.

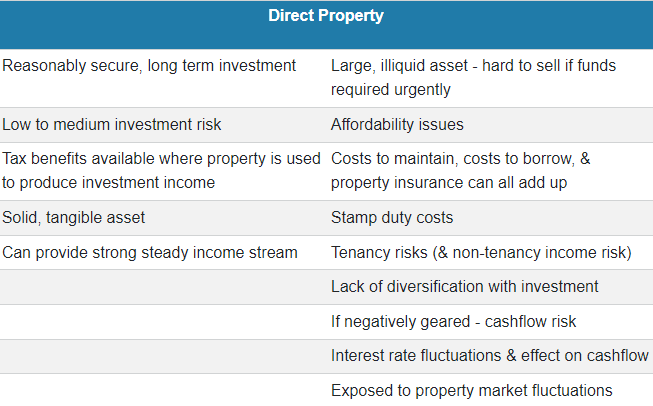

Investing in Direct Property: The Gearing Powerhouse

Property is often viewed as a "safe as houses" investment. It is a solid, tangible asset that many Australians understand instinctively. In 2026, despite higher interest rates compared to the previous decade, the national housing shortage continues to drive capital growth in key markets.

The Benefits of Property

Leverage (Gearing): You can typically borrow 80% or more of a property's value. If a $1,000,000 property grows by 5%, you have made $50,000 on your initial $200,000 deposit, a 25% return on your equity.

Tax Deductions: Property investors can access significant deductions via depreciation, interest costs, and general upkeep.

Stability: Unlike the daily fluctuations of the ASX, property prices are not updated by the minute, which can prevent emotional "panic selling" during market turbulence.

The 2026 Property Landscape

It is important to note that property is not a single market. While Sydney and Melbourne often lead in value, cities like Perth and Brisbane are currently experiencing double-digit growth due to acute supply constraints. However, investors must be wary of new regulatory changes. For instance, the ATO has recently tightened rules regarding holiday home tax deductions, specifically targeting "leisure facilities" used for personal recreation.

Comparing the Challenges

Both asset classes come with their own set of hurdles that must be managed through professional market research.

Borrowing to Invest: A Double-Edged Sword

Most property investors use negative gearing, where the cost of borrowing exceeds the rental income. This loss can be used to reduce your taxable income. While popular, this requires significant cash flow from other sources (like your salary) to service the debt. In contrast, borrowing to invest in shares via a margin loan can also magnify returns, but carries the risk of a margin call if the market dips suddenly.

Practical issues

For borrowing to be appropriate, the following general conditions are recommended:

- The investor should have sufficient income to meet the expenses arising from the investment, including loan repayments, maintenance fees, insurance etc.

- The investor generally needs to own other assets which can be offered as security for the loan.

- The investment should have the potential for income and capital growth.

- Commonly, investment loans are interest-only to obtain the maximum tax advantage, however, principal & interest repayments may be required (SMSFs owning property are now required to make P&I repayments, for example).

- Accept that the strategy provides maximum return over a longer time period.

- Recognise that borrowing increases both potential return and risk.

- Borrowing to invest produces a specific obligation to service a debt. One of the critical elements of this type of strategy is to ensure continuity of income. Income protection insurance should be maintained by the investor in this regard.

Risks associated with borrowing

- Investment income risk: if investment income is lower than expected or does not grow as expected, the negative cashflow will be larger than expected and continue for longer. Negative cash flow needs to be covered by income from other sources (usually salary).

- Risk of capital loss: if the capital value reduces and the investment is sold, the proceeds may not cover the loan. The remaining loan balance will need to be repaid from other assets.

- Interest rate risk: interest rates on the loan may rise, increasing the negative cash flow needing to be covered from other sources. This risk can be managed by using fixed rate loans if applicable.

- Income risk: normal living costs still need to be met as well as the negative cashflow. What contingency plans does the investor have if salary is reduced overtime, or income ceases because of redundancy, sickness or injury, or death of the investor or their partner? Income and living costs can change following the ending of a relationship, separation or divorce.

Many of the risks arising from a reduction in income should be fully covered by insurance. Insurance should cover death, permanent and temporary disablement and most importantly, income protection. Insurance should not only cover the investor but also the partner, if applicable, as a significant change in the partner's circumstances can also significantly affect surplus cash flow available to cover negatively geared investments.

Everyone will have their own opinion as to which investment strategy is best. For many Australians, property ownership is a rite of passage. However, shares can never be overlooked as a convenient, tax effective long-term solution to generate income and wealth.

For investors approaching retirement, holding an overweight position in direct property may not be the best strategy given investment needs change in retirement.

The Hybrid Approach: Why Choose?

The most successful portfolios often combine both asset classes. Property provides the stability of a tangible asset and the power of leverage, while shares provide liquidity, diversification, and the unique tax benefits of franking. As you approach retirement, your needs change; holding an overweight position in illiquid property can make it difficult to fund your daily lifestyle.

A balanced investment strategy ensures you have the growth of the share market and the security of real estate, protected by a layer of professional oversight.

Navigating the choice between shares and property requires a deep understanding of your risk profile and long-term goals. Whether you are looking to build a high-yield dividend portfolio or secure your first investment property, our team is here to guide your decision.

Contact a Morgans adviser today to review your asset allocation or find a financial adviser at a branch near you to discuss your wealth goals.

Frequently Asked Questions

Is property safer than shares in 2026?

Property is often perceived as "safer" because it is tangible, but it is also highly leveraged and illiquid. Shares are more volatile in the short term, but they offer greater diversification and the ability to exit your position instantly if your circumstances change.

What is the long-term return of the ASX vs property?

Historically, the Australian share market has delivered total returns (growth plus dividends) of around 9–11% per annum over the long term. Property returns vary significantly by location but often average around 6–8% plus rental income, though leverage can significantly increase the return on your initial cash investment.

Can I buy property within my SMSF?

Yes, an SMSF can purchase direct property. However, there are strict rules: the property must meet the "sole purpose test" and cannot be lived in by you or a related party. Many investors use this to hold business real property for their own companies.

Are franking credits still a reliable tax benefit?

Yes, the dividend imputation system remains a fundamental part of the Australian tax landscape. While there is ongoing political debate about the refundability of excess credits, they remain a powerful tool for reducing the effective tax rate on your investment income.

Should I pay off my mortgage or invest in shares?

This depends on your interest rate and tax bracket. Paying off a non-deductible home loan provides a guaranteed "return" equal to the interest saved. However, if your investment in shares (after tax and franking) is expected to outperform your mortgage rate, investing the surplus cash may build wealth faster over time.