This article is a reworking of Michael Knox’s full presentation, to view the un-edited presentation, please view the video above.

Key summaries

- Australia is likely to face higher inflation driven by electricity and oil prices

- Economists expect two to three RBA rate hikes through the rest of the year

- Higher interest rates normally raise recession risks, but this cycle is different

- Stronger export prices are providing a powerful offset to domestic weakness

- Elevated energy prices will support Australia’s commodity income for longer

Introduction

In recent days, pessimism about the Australian economic outlook has intensified. Rising inflation, driven by structural pressures in electricity prices and renewed strength in oil markets, has led many economists to forecast further interest rate hikes from the Reserve Bank of Australia.

Under normal circumstances, multiple rate rises would significantly increase the risk of an economic slowdown or recession. Yet this time, the outlook may be more resilient than many expect. The key variable is Australia’s export performance and the global forces driving commodity prices higher.

Inflation pressures remain structurally higher in Australia

Australia’s inflation challenge is not simply a short-term supply shock. Structural factors continue to place upward pressure on prices, particularly in energy and electricity. Domestic electricity pricing remains elevated. While higher oil prices attract most headlines, electricity costs feed directly into household expenses and business operating costs, keeping inflation higher even as demand moderates. As a result, markets increasingly expect the RBA to respond with further tightening. Current consensus suggests two, and possibly three, additional rate hikes over the balance of the year.

Interest rate hikes and the usual recession risk

Traditionally, rising interest rates suppress consumption, slow housing markets and reduce business investment. In most economic cycles, this combination materially increases recession risk within 12 to 18 months. But this cycle differs from previous rate-hiking periods because Australia is receiving a significant income boost from global commodity markets.

Export prices are offsetting domestic tightening

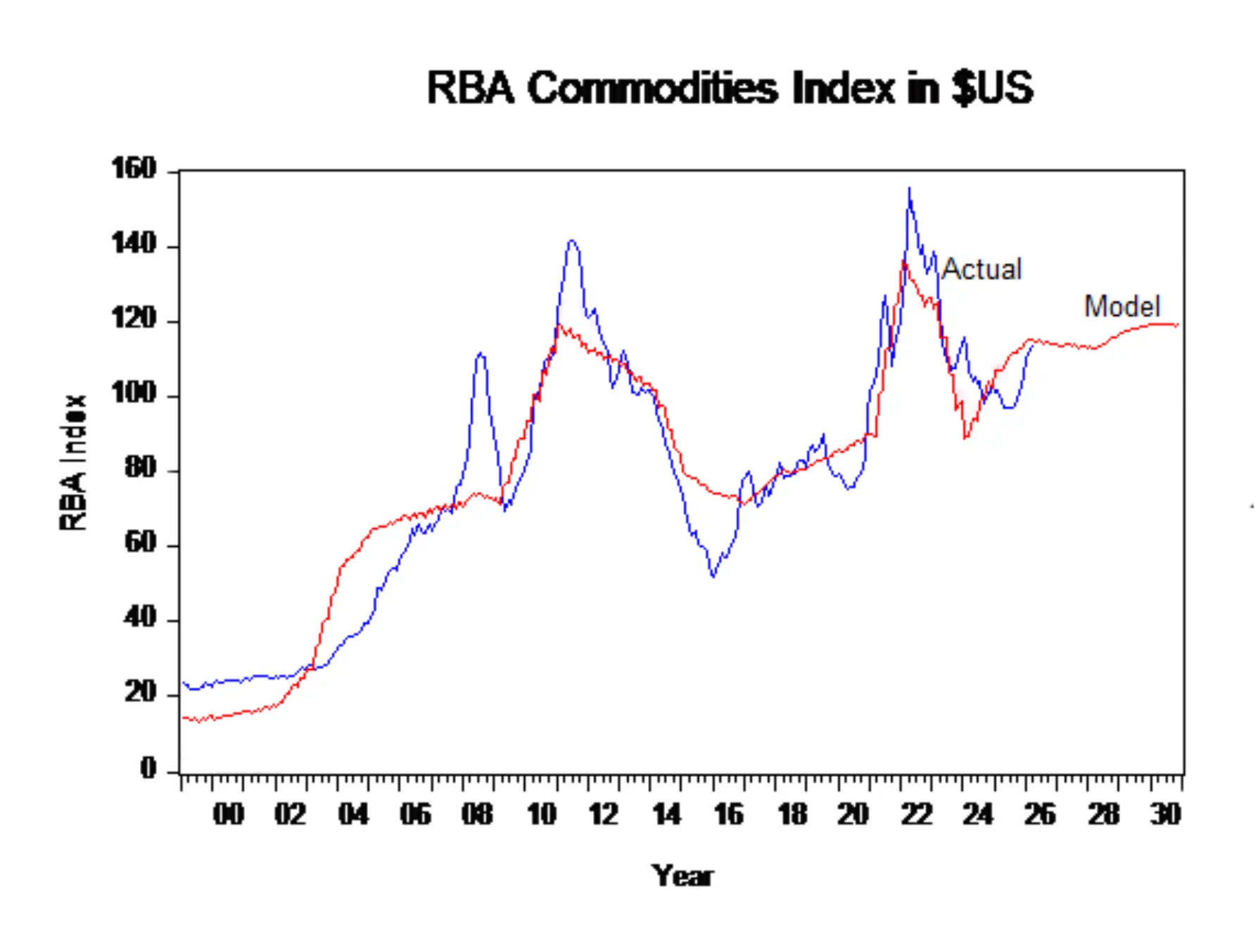

Australia’s export sector remains a critical stabiliser. One of the clearest indicators is the RBA commodities index measured in US dollar terms. Our model explains 88% of monthly variation in this Index . Australian Export Prices have risen 18% since last June . Our model tells us this strength will continue. High Export prices flow through as higher domestic income. Periods when export prices overshoot the model are typically explained by higher energy prices. Right now, oil prices are leading to higher LNG prices and higher coal prices.

Oil price strength and the Middle East supply shock

According to the OPEC Monthly Oil Market Report released in April, there has been a significant slump in crude oil deliveries to refineries. The reported decline is approximately five million barrels per day. On a monthly basis, this equates to around 150 million barrels of oil that are no longer flowing into refineries globally. This is an enormous supply shortfall. Lower refinery throughput means reduced production of refined petroleum products such as petrol, diesel and jet fuel. As these stocks decline, prices move higher. Historical evidence shows a clear relationship. When inventories of refined petroleum products fall, oil prices rise. When inventories build, prices tend to fall. At present, stocks are falling and the process has only just begun.

Why oil prices may stay higher for longer

Oil prices may remain above US$100 per barrel through the end of this year, before easing sometime in the following year.

What this means for Australia’s economy

- Higher oil prices will lead to higher prices for Australian LNG and coal exports

- This higher export income acts as a buffer against domestic tightening.

- It helps offset the drag from higher interest rates, supporting employment, investment and national income.

Implications for investors

Energy producers and commodity exporters are positioned to benefit from sustained strength in oil prices.

Conclusion

Australia is facing a challenging inflation environment, with electricity and oil prices driving expectations of further interest rate rises. Ordinarily, this would heighten recession risk. However, with energy prices likely to remain elevated due to supply constraints and Middle East tensions, Australia’s external earnings will support the economy through this tightening cycle.

Call to action

To understand how these economic forces may affect your portfolio and investment strategy, speak with a Morgans adviser today or explore our latest market insights.

Frequently asked questions

Why is inflation structurally higher in Australia?

Australia’s inflation is driven by persistent electricity costs, energy transition challenges and global oil price strength rather than short-term demand factors.

How many interest rate hikes are expected in Australia this year?

Most economists currently expect two to three additional rate hikes over the remainder of the year.

Why might Australia avoid a recession despite higher rates?

Strong export prices and commodity income are helping offset domestic economic tightening.

What is driving oil prices higher?

Falling refinery supply, declining petroleum stocks and Middle East geopolitical tensions are pushing prices higher.

Will oil prices fall soon?

Oil prices are expected to remain elevated through the end of the year, with declines more likely sometime next year.

Want to discuss how this impacts your portfolio?

DISCLAIMER: Information is of a general nature only. Before making any financial decisions, you should consult with an experienced professional to obtain advice specific to your circumstances.