- Morgans research analysts re-set their sector views, strategies and best ideas as dynamic forces continue to challenge markets.

- Our approach in equities currently favours stocks with compelling risk/reward profiles among quality cyclicals and select mid-to-small caps.

- Preferred equity sectors include staples, healthcare and financials along with select travel exposure.

Our base case remains a cyclical slowdown / mild recession

Our Asset Allocation Update – 2024 Outlook discusses three possible economic scenarios in 2024 and their investment implications in terms of portfolio asset allocation. Our base case scenario expects economic growth to contract in the first half of 2024 before returning to growth later in the year. Sticky inflation will keep interest rates higher for longer. Equities will likely remain rangebound until there is more certainty on the interest rate trajectory either peaking/falling.

This scenario could have an interesting dynamic around small and mid-cap stocks. These companies were derated in 2023 as they grappled with higher interest rates, and their risk-reward profile looks attractive despite the recession risks. With central banks on high alert for persistent inflation, short-dated, high-quality credit should form the core part of the fixed income allocation. A mild recession would be positive for property because a small amount of inflation is positive for real estate. Furthermore, REIT prices have declined materially, which could lead to opportunities in areas that investors have overlooked in 2023 (retail/commercial REITs).

Given Australia’s economic sensitivity to falling commodity prices, investors need to tread carefully over the next 3-6 months. As tailwinds from commodity prices fade, we think above-average earnings growth for the market will be harder to come by. Accordingly, we prefer a targeted portfolio approach, tilting toward what we believe are the best relative opportunities and the best risk/return profile e.g., small caps, quality cyclicals.

Morgans sector analysts have downgraded their rating on the Telco sector to Slightly Underweight (from Neutral). Telco sits in the expensive defensive basket with the positives looking priced in. The sector could easily see downside risks, potentially as a funding source for a rotation into growth sectors in 2024.

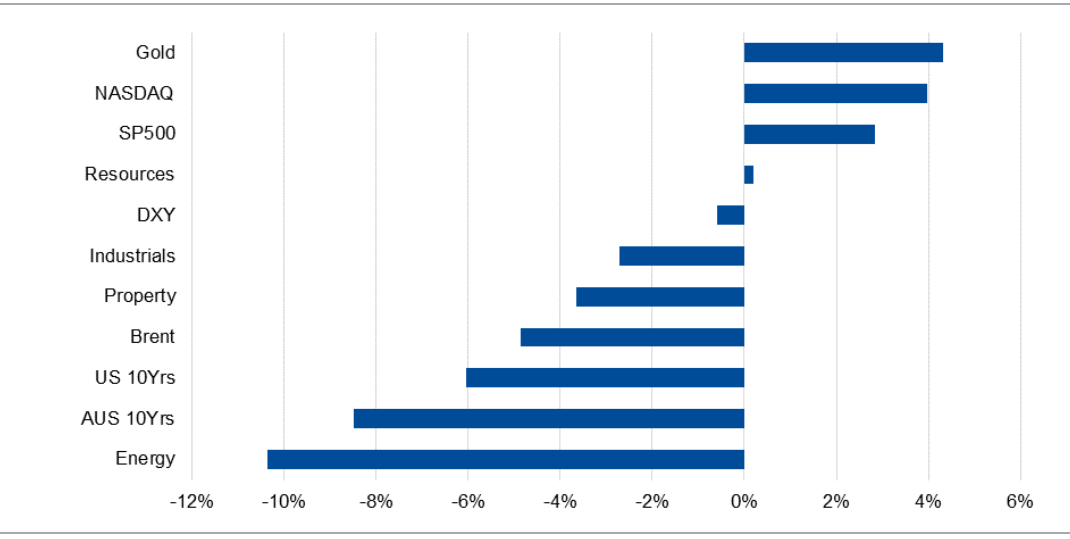

Relative 3-month asset class performances

Morgans clients receive access to detailed market analysis and insights, provided by our award-winning research team. Begin your journey with Morgans today to view the exclusive coverage.