On 7 July the AFR published a list of 37 Economists who had answered a poll on when the RBA would next cut rates. 32 of them thought that the RBA would cut on 8 July. Only 5 of them did not believe the RBA would cut on 8 July. I was one of them. The RBA did not cut.

So today I will talk about how I came to that decision. First, lets look at our model of official interest rates. Back in January 2015 I went to a presentation in San Franciso by Stan Fishcer . Stan was a celebrated economist who at that time was Ben Bernanke's deputy at the Federal Reserve. Stan gave a talk about how the Fed thought about interest rates.

Stan presented a model of R*. This is the real short rate of the Fed Funds Rate at which monetary policy is at equilibrium. Unemployment was shown as a most important variable. So was inflationary expectations.

This then logically lead to a model where the nominal level of the Fed funds rate was driven by Inflation, Inflationary expectations and unemployment. Unemployment was important because of its effect on future inflation. The lower the level of unemployment the higher the level of future inflation and the higher the level of the Fed funds rate. I tried the model and it worked. It worked not just for the Fed funds rate. It also worked in Australia for Australian cash rate.

Recently though I have found that while the model has continued to work to work for the Fed funds rate It has been not quite as good in modelling that Australian Cash Rate. I found the answer to this in a model of Australian inflation published by the RBA. The model showed Australian Inflation was not just caused by low unemployment, It was also caused by high import price rises. Import price inflation was more important in Australia because imports were a higher level of Australian GDP than was the case in the US.

This was important in Australia than in the US because Australian import price inflation was close to zero for the 2 years up to the end of 2024. Import prices rose sharply in the first quarter of 2025. What would happen in the second quarter of 2025 and how would it effect inflation I could not tell. The only thing I could do is wait for the Q2 inflation numbers to come out for Australia.

I thought that for this reason and other reasons the RBA would also wait for the Q2 inflation numbers to come out. There were other reasons as well. The Quarterly CPI was a more reliable measure of the CPI and was a better measure of services inflation than the monthly CPI. The result was that RBA did not move and voiced a preference for quarterly measure of inflation over monthly version.

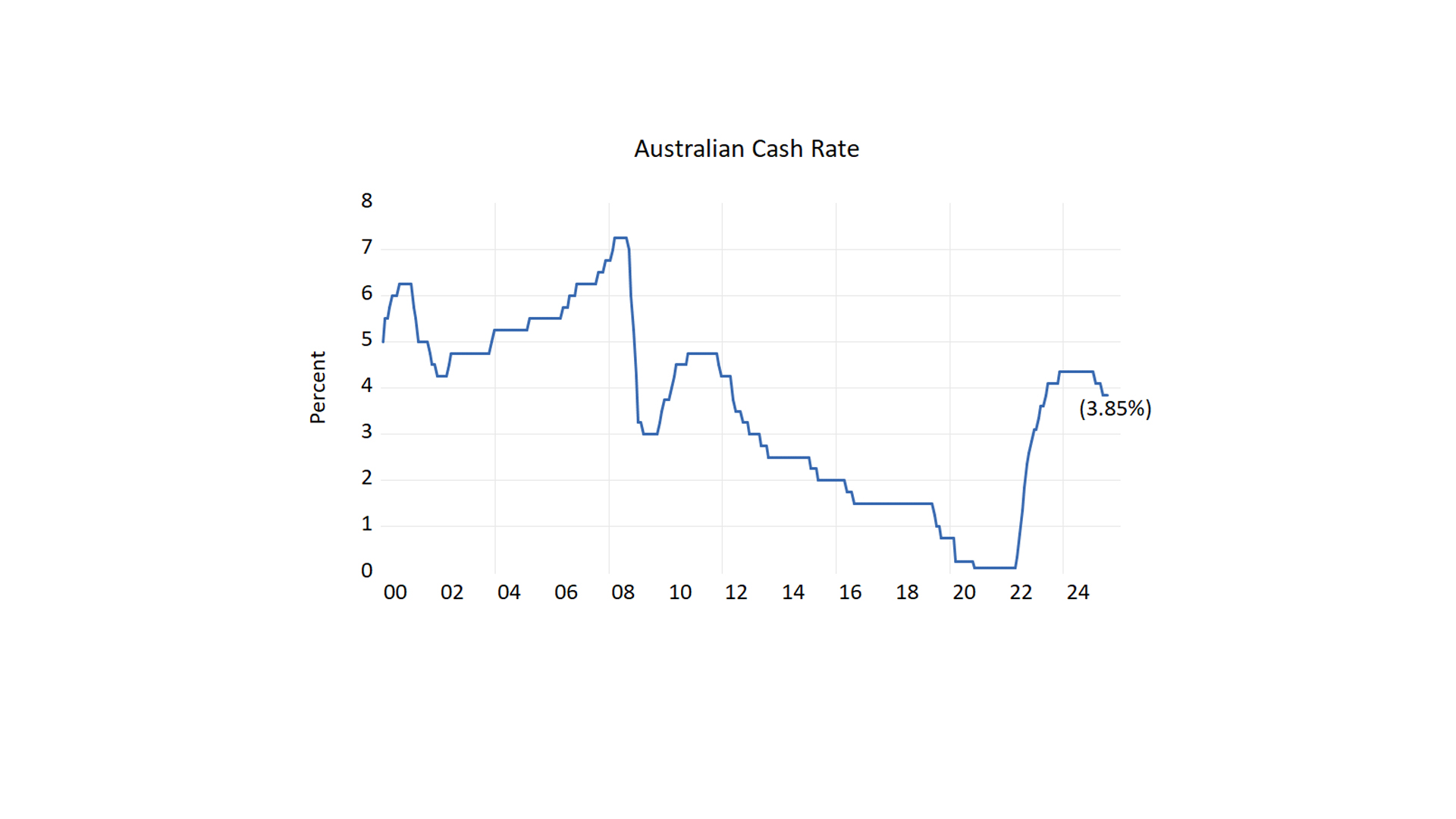

Lets look again at R* or the real level of the Cash rate for Australia .When we look at the average real Cash rate since January 2000 we find an average number of 0.85%. At an inflation target of 2.5 % this suggests this suggest an equilibrium Cash rate of 3.35%

What will happen next? We think that the after the RBA meeting of 11 and 12 August the RBA will cut the Cash rate to 3.6%

We think that after the RBA meeting of 8 and 9 December the RBA will cut the Cash rate to 3.35%

Unless Quarterly inflation falls below 2.5% , the Cash rate will remain at 3.35% .