We think the US economy is currently experiencing solid growth, with data from the Chicago Fed National Activity Index indicating an annual growth rate of just above 2%. This aligns with projections from other parts of the Federal Reserve System, such as the New York Fed. The New York Fed’s weekly Nowcast, updated every Friday, estimates that for the second quarter of 2025, the US economy is growing at an annualised rate of 2.34%, surpassing the 2% mark. This robust growth is consistent with our model’s view that the US economy is now performing strongly. However, we anticipate a slowdown in the second half of 2025.

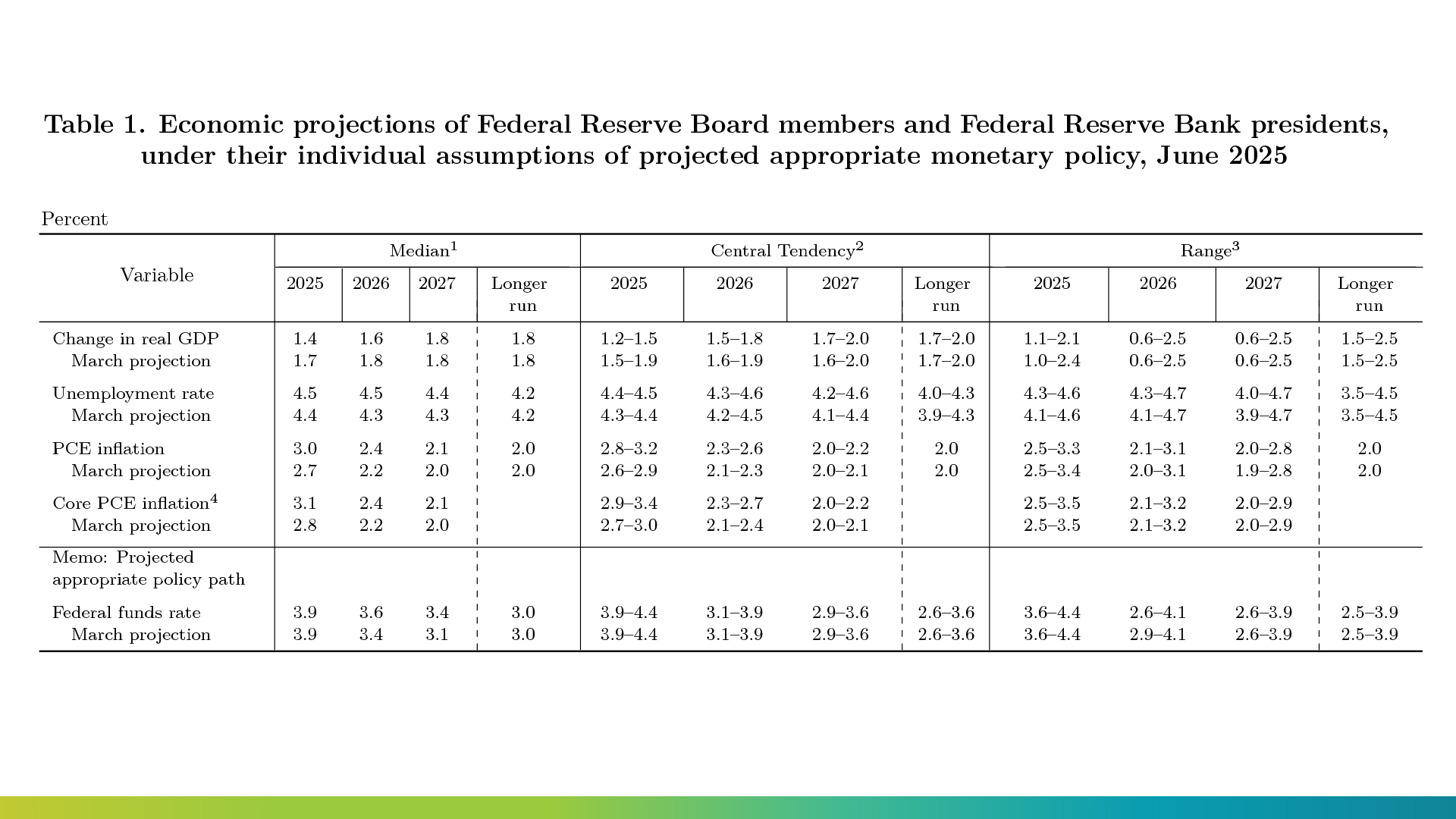

On 18 June the Fed released its Summary of Economic Projections with the Federal Reserve’s forecasting US GDP growth to drop to 1.4% in 2025, down from their March estimate of 1.7%. Looking further ahead, growth is expected to pick up slightly to 1.6% in 2026 and 1.8% in 2027, aligning with the long-term trend growth rate of around 1.8%. We believe this recovery trend could be even higher, driven by reduced regulation under the second Trump administration and aggressive tax write-offs for companies building factories in the US, allowing 100% write-offs for equipment and buildings in the first year. This policy should foster stronger systemic growth.

The Fed expects that as the economy slows, unemployment is projected to rise to 4.5% from the current level of 4.2%. Inflation, measured by the Consumer Price Index (CPI), is running at 3.5% this year, approximately 50 basis points higher than the Personal Consumption Expenditures (PCE) index of 3.0%, with 1.6% of this inflation attributed to tariffs. The Fed expects PCE Inflation to ease to 2.4% in 2026 and 2.1% in 2027. The Federal Reserve anticipates cutting the effective federal funds rate, currently at 433 basis points (according to the New York Fed), by 50 basis points by the end of 2025, followed by an additional 25 basis points in each of the next two years. This aligns with our own Fed Funds rate model’s current equilibrium federal funds rate of 3.85% . The Fed Outlook supports our scenario of a slowing US economy and rate cuts in the second half of 2025 and beyond. A falling US dollar is then expected to exert upward pressure on commodity prices, benefiting Australian Equity markets.

Taking questions during the Press Conference after releasing the Fed statement ,Federal Reserve Chair Jay Powell, addressed the certainty and uncertainty surrounding the inflationary effects of tariffs. Initially, at the start of 2025, the inflationary impact of tariff policies was unclear, but three months of favourable inflation data have provided this clarity, indicating that the inflationary effects are less severe than anticipated. Powell noted that the Feds own uncertainty on the inflationary effects of tariffs peaked in April 2025, and the Federal Reserve now has a clearer understanding that the inflation effects, are lower than initially expected.

The Fed view supports our own scenario of a slowing US economy in the second half of 2025, allowing for Fed rate cuts . This in turn should then lead to a falling US dollar, which we in turn expect to drive rising commodity prices.