This article is a reworking of Michael Knox’s full presentation, to view the un-edited presentation, please view the video above.

Key takeaways

- Recent oil price falls have been driven by peace headlines, not an immediate improvement in supply

- Global oil stock levels remain low after weeks of disruption through the Strait of Hormuz

- Markets have reacted to misinformation around Iran’s negotiations, amplifying volatility

- Official modelling suggests oil prices may take until early next year to reach lower levels

- Elevated oil prices may persist even in a stable geopolitical environment

Introduction

Oil prices have fallen sharply in recent days, driven by optimism around a ceasefire in the Middle East and renewed negotiations between the United States and Iran. Headlines have pointed to peace, diplomacy, and the prospect of oil supply returning to global markets.

But beneath the surface, the outlook for oil prices is far more complex.

Misreporting around Iran’s negotiations, ongoing supply disruptions through the Strait of Hormuz, and critically low global oil stock levels are creating conditions that could keep oil prices higher for longer than many investors expect. Even if tensions continue to ease, history and modelling suggest any decline in oil prices is likely to be slow, not sudden.

Here is what is really happening in global oil markets and what it means for prices over the next 12 to 18 months.

Media confusion has distorted oil market sentiment

In recent days, several major media outlets reported on what they described as Iran’s ten point negotiation plan with the United States. These reports included claims that Iran proposed imposing transit fees of around US$2 million per ship passing through the Strait of Hormuz.

The problem is that this claim did not appear in Iran’s actual ten point plan.

Instead, it emerged from an AI generated summary that incorrectly described one of the items. When the official Iranian document was released through state affiliated channels, it became clear that item ten focused on ceasing hostilities, including in Lebanon, not the introduction of transit fees.

Despite this correction, the initial claims were widely circulated, criticised by commentators, and factored into market sentiment. This highlights how quickly misinformation can influence commodity pricing, particularly when tensions in key supply regions are involved.

Why the Strait of Hormuz still matters for oil prices

While headlines focused on negotiations, a more important development was unfolding quietly in the background.

Because of the War, shipping through the Strait of Hormuz was effectively halted for around six weeks.

During this period:

- Oil deliveries were delayed or diverted

- Global stockpiles were drawn down

- Supply tightened relative to demand

In normal conditions, global oil markets operate with approximately 100 days of stock coverage. However, when a major transit route closes for weeks at a time, those stock levels fall quickly.

Even if shipping resumes, rebuilding inventories takes time. This lag effect is critical to understanding why oil prices may remain elevated even as geopolitical tensions ease.

What US–Iran negotiations actually mean for oil supply

The war began because of Iranian Statements to US Negotiators Steve Witkoff and Jared Kushner that Iran had enough enriched uranium to almost immediately build 11 nuclear weapons. Source: Trump’s 11 Nuclear Reasons for the Iran War. US negotiators currently believe that they will gain possession of all Iranian enriched Uranium. The United States is monitoring by satellite all enriched uranium facilities that were bombed last year. The US believes that this enriched uranium will be removed and no future enrichment permitted.

From an oil market perspective, this signals a path toward stability rather than an immediate surge in supply.

Why oil prices fall slowly, not suddenly

The relationship between oil stocks and prices works much like the labour market:

- When labour supply is tight, wages rise quickly

- When oil supply is tight, prices rise sharply

- When supply improves, adjustments occur gradually

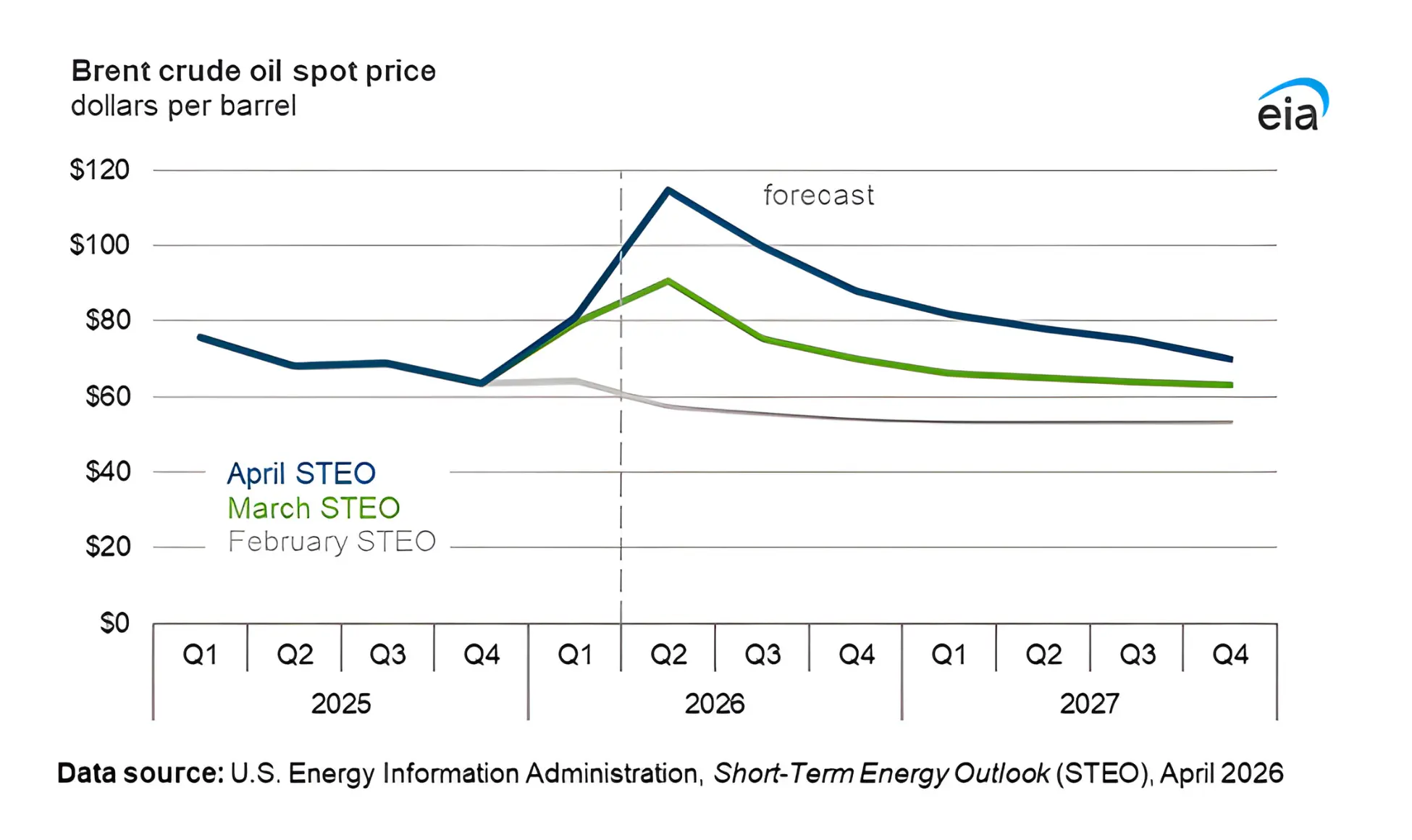

Recent modelling from the US Energy Information Administration has explored a scenario where peace breaks out immediately. Even under this assumption, price declines are slow.

Their projections show oil prices easing gradually toward around US$80 per barrel only by the end of the first quarter next year. From there, prices fall further toward roughly US$70 per barrel by the end of 2027

This slow adjustment reflects the time needed to rebuild inventories and restore normal supply chains.

The long term real price of oil remains elevated

Looking beyond short term headlines, history provides useful context.

Real oil prices, adjusted for inflation, have averaged around US$89 per barrel over the long term since the 1970s. This suggests that even what feels like a high nominal price today is not historically unusual once inflation is considered.

When combined with:

- Lower global stock levels

- Ongoing geopolitical risk

- Gradual supply normalisation

It becomes clear why current oil prices may remain supported for longer than expected, even in a calmer world.

What this means for investors and oil stocks

For investors, the key takeaway is that recent events do not necessarily signal the end of elevated oil prices.

While short term volatility has increased, the structural backdrop still points to:

- Tight supply conditions

- Slow inventory rebuilds

- A prolonged adjustment period

For those holding oil related investments, High prices may persist longer than headlines imply.

FAQs

Why did oil prices fall so sharply recently?

Oil prices fell due to optimism around peace talks and media reports suggesting improved supply conditions, even though actual oil flows have not yet recovered.

Is the Strait of Hormuz still affecting oil supply?

Yes. Disruptions lasted for weeks, reducing global stock levels. Even with reopening, inventories take time to rebuild.

Will US–Iran negotiations flood markets with oil?

No . Diplomacy does not immediately translate into higher production or exports.

When are oil prices expected to fall meaningfully?

Current modelling suggests prices may not reach lower levels until early next year, with gradual declines through the year after.

Are current oil prices historically high?

In real terms, current prices are only modestly higher than long term averages rather than extremely high.

Conclusion and next steps

Despite recent falls, the oil prices outlook remains shaped by constrained supply, depleted stock levels, and slow moving structural forces. Peace headlines alone are not enough to undo weeks of disruption or decades of pricing behaviour.

For investors, understanding what is driving oil prices beneath the surface is critical. Markets may continue to react to news flow, but fundamentals suggest elevated prices could persist longer than many expect.

Want to discuss how this impacts your portfolio?

DISCLAIMER: Information is of a general nature only. Before making any financial decisions, you should consult with an experienced professional to obtain advice specific to your circumstances.