I’d like to discuss a presentation delivered by Austan Goolsbee, President of the Federal Reserve Bank of Chicago, to the Economic Club of New York on 10 April. Austan Goolsbee, gave a remarkably animated talk about tariffs and their impact on the U.S. economy.

Goolsbee is a current member of the Federal Reserve’s Open Market Committee, alongside representatives from Washington, D.C., and Fed bank Presidents from Chicago, Boston, St. Louis, and Kansas City.

Having previously served as Chairman of the Council of Economic Advisers in the Obama White House, Goolsbee’s presentation style in New York was notably different from his more reserved demeanour I had previously seen when I had attended a talk of his in Chicago.

During his hour-long, fast-paced talk, Goolsbee addressed the economic implications of tariffs. He recounted an interview where he argued that raising interest rates was not the appropriate response to tariffs, a stance that led some to label him a “Dove.” He humorously dismissed the bird analogy, instead likening himself to a “Data Dog,” tasked with sniffing out the data to guide decision-making.

Goolsbee explained that tariffs typically drive inflation higher, which might ordinarily prompt rate hikes. However, they also tend to reduce economic growth, suggesting a need to cut rates. This creates a dilemma where rates might not need adjustment at all. He described tariffs as a “stagflation event” but emphasised that their impact is minor compared to the severe stagflation of the 1970s.

When asked if the U.S. was heading towards a recession, Goolsbee said that the "hard data" was surprisingly strong.

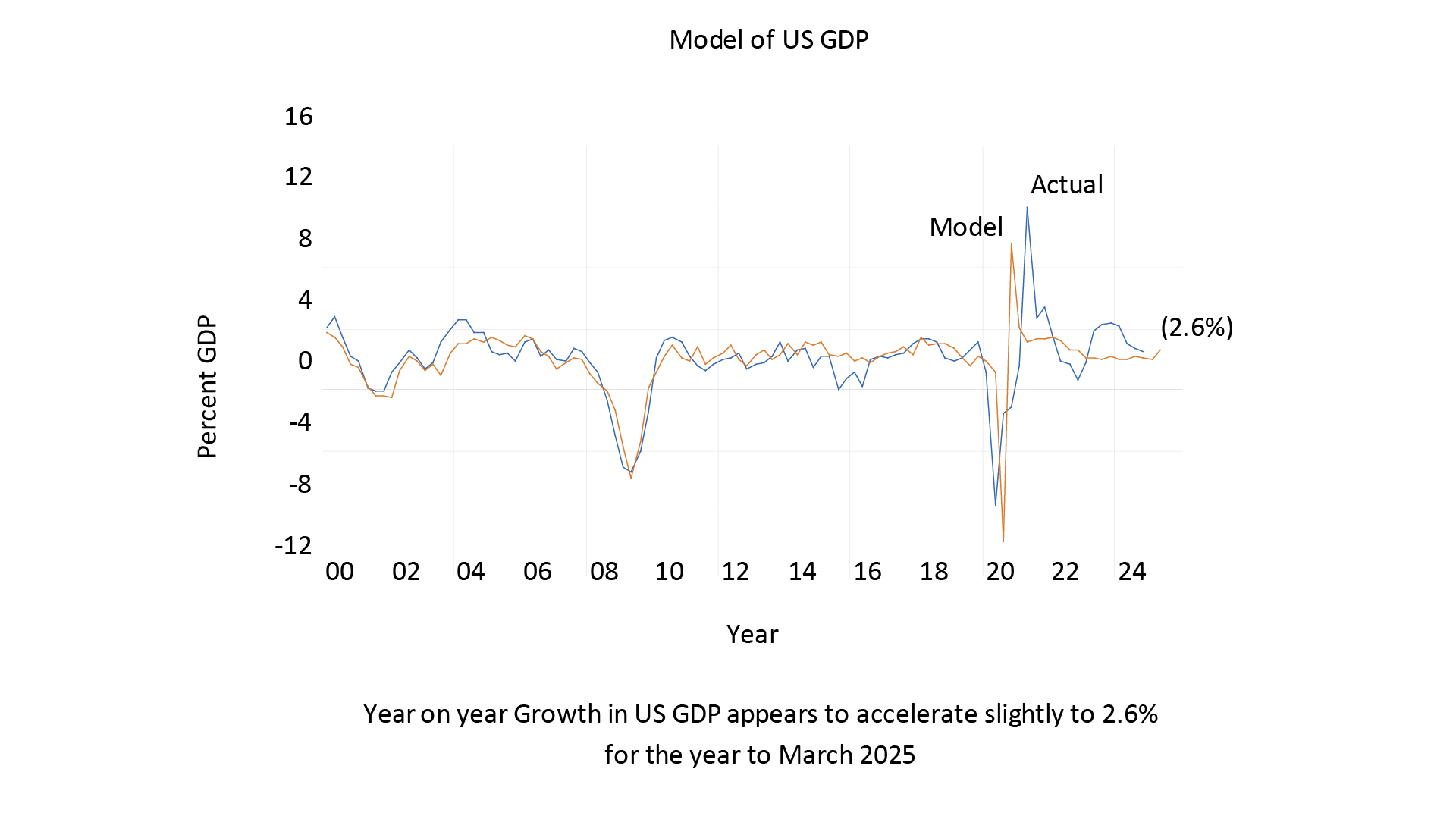

Let us now look at our model of US GDP based on the Chicago Fed National Activity Index. This Index incorporates 85 variables across production, sales, employment, and personal consumption. In the final quarter of last year, this index indicated the GDP growth was slightly below the long-term average, suggesting a US GDP growth rate of 1.9% to 2%.

However, data from the first quarter of this year showed stronger growth, just fractionally below the long-term trend.

Using Our Chicago Fed model, we find that US GDP growth had risen from about 2% growth to a growth rate of around 2.6%, indicating a robust U.S. economy far from recessionary conditions.

We think that increased government revenue from Tariffs might temper domestic demand, potentially guiding growth down towards 1.9% or 2% by year’s end. Despite concerns about tariffs triggering a downturn, this highlights the economy’s resilience and suggests a “soft landing,” which could allow interest rates to ease, weaken the U.S. dollar, and boost demand for equities.

We will provide monthly reviews of these indicators. We note that, for now, the outlook for the U.S. economy remains very positive.