In the 1930s, US Treasury Secretary Henry Morgenthau was widely regarded as the finest Treasury Secretary since Alexander Hamilton. However, if the current Treasury Secretary Scott Bessent continues to deliver results as he is doing now, he will provide formidable competition to Morgenthau’s legacy.

The quality of Bessent’s work is exceptional, demonstrated by his ability to secure an agreement with China in just a few days under complex circumstances.

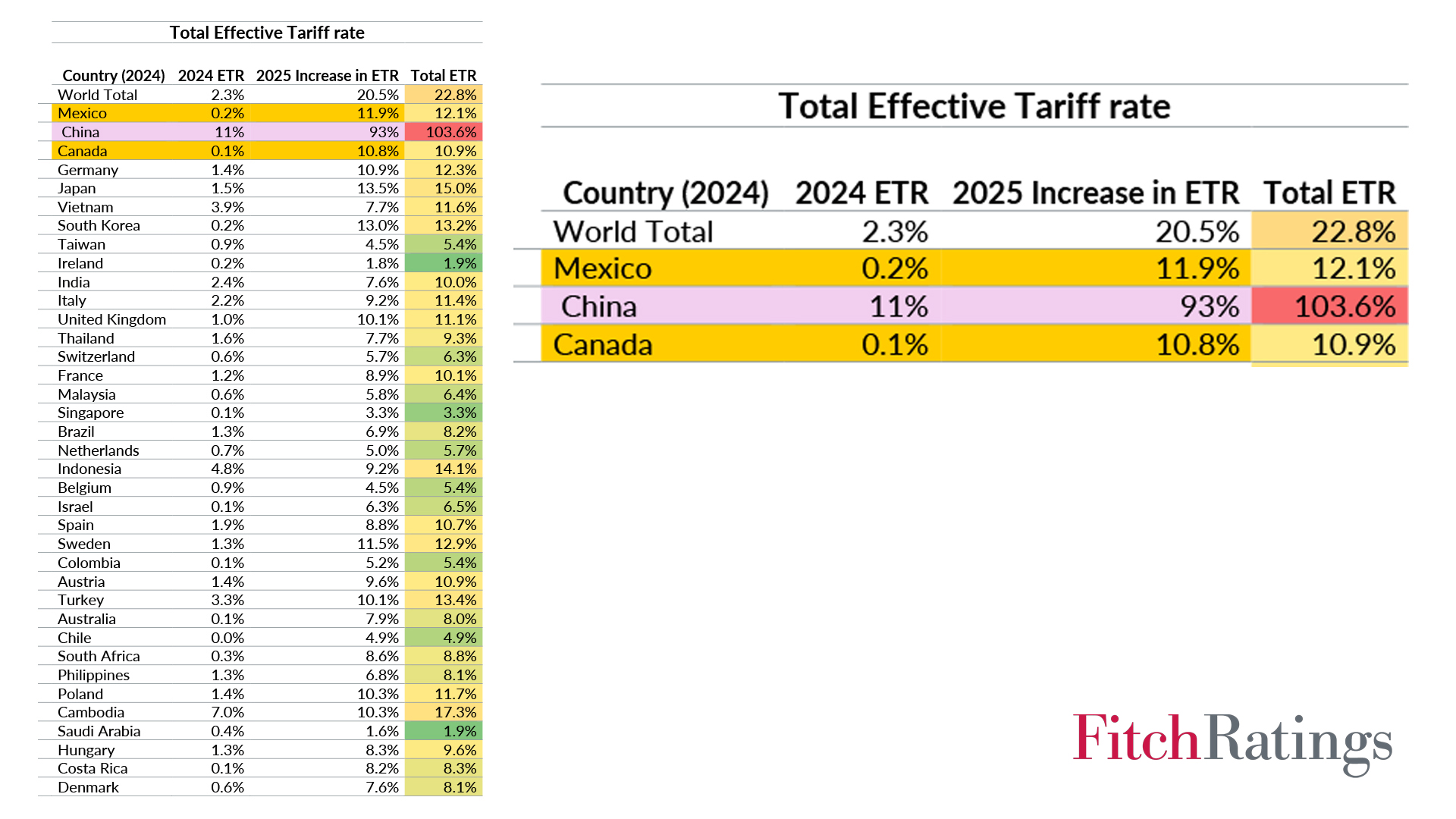

Understanding the Effective Tariff Rate

The concept of the effective tariff rate has gained traction recently. Although nominal tariff rates on individual goods in some countries can be as high as 100 or even 125 percent, the effective tariff rate, which reflects the actual tariffs the US imposes on imports from all countries, is thought to be only 20.5 percent. This figure comes from an online spreadsheet published by Fitch Ratings on 24 April.

This effective tariff rate of 20.5 percent can be used to assess the impact of import tariffs on US inflation. To evaluate this, I used a method proposed by Scott Bessent during his Senate confirmation hearing. Bessent noted that imports account for only 16 percent of US goods and services consumed in the economy. In this case, a 10 percent revenue tariff would increase domestic prices by just 1.6 percent. With a core inflation rate of 2.8 percent in the US, this results in a headline inflation rate of 4.4 percent. The overall impact of such tariffs on the US economy is relatively modest.

Tariffs and the Federal Reserve

A couple of weeks ago, Austan Goolsbee, President of the Chicago Fed, noted that tariffs typically increase inflation, which might prompt the Fed to lift rates, but they also reduce economic output, which might prompt the Fed to cut rates. Consequently, Goolsbee suggested that the Federal Reserve might opt to do nothing. This prediction proved correct when the Open Market Committee of the Fed, with Goolsbee as a member, left the Fed Funds rate unchanged last week.

The US-China Agreement

A 90-day agreement between the US and China, negotiated by Scott Bessent, has dramatically reduced tariffs between the two countries. China now imposes a 10 percent import tariff on the US, while the US applies a 30 percent tariff on Chinese goods: 10 percent as a revenue tariff and 20 percent to pressure China to curb the supply of fentanyl ingredients to third parties in Mexico or Canada. Fentanyl fuels the US drug crisis, making this a priority for the Trump administration.

How Import Tariffs Affect US Inflation

We can calculate how much inflation a tariff adds to the US economy using Bessent’s method by multiplying the effective tariff rate by the proportion that imports represent in US GDP. Based on a 20.5 percent effective tariff rate, I calculated that it adds 3.28 percent to the US headline Consumer Price Index (CPI). This results in a US headline inflation rate of 6.1 percent for the year ahead.

In Australia, we can draw parallels to the 10 percent GST introduced 24 years ago, where price effects were transient and vanished after a year, avoiding sustained high inflation.

Before these negotiations, the US was levying a nominal tariff on China of 145 percent. Some items were not taxed, so the effective tariff on China was 103 percent. Levying this tariff meant that the US faced a price effect of 3.28 percent, contributing to a 6.1 percent headline inflation rate.

If the nominal tariff rate dropped to 80 percent, the best-case scenario I considered previously, the price effect would fall to 2.4 percent, with a headline US inflation rate of 5.2 percent. With the US now charging China a 30 percent tariff, this adds only 2 percent to headline inflation, yielding a manageable 4.8 percent US inflation rate.

As Goolsbee indicated, the Fed might consider raising interest rates to counter inflation or cutting them to address reduced output, but ultimately, it is likely to maintain current rates, as it did last week. I anticipate the Fed will continue to hold interest rates steady but with an easing bias, potentially cutting rates in the second half of the year once the situation stabilises.

My current Fed Funds rate model suggests that, absent this year’s tariff developments, the Fed would have cut rates by 50 basis points. This could be highly positive for the US economy.