Today, I’m presenting the first page of my updated presentation, which focuses on GDP growth and inflation expectations for major economies. Before diving into that, I want to clarify a point about U.S. trade negotiations that has confused some media outlets.

In the previous Trump Administration ,there was single trade negotiator, Robert Lighthizer, held a cabinet position with the rank of Ambassador. This time, to expedite negotiations and give them more weight, Trump has appointed two additional cabinet-level officials to handle trade talks with different regions. For Asian economies, Scott Bessent and Ambassador Jamison Greer, who succeeded Lighthizer and previously served on the White House staff, are managing negotiations, including those with China. For Europe, Howard Lutnick, the Commerce Secretary, and Ambassador Greer are negotiating with the European Trade Representative. When the EU representative visits Washington, D.C., they meet with Lutnick and Greer, while Chinese or Japanese representatives engage with Bessent and Greer.

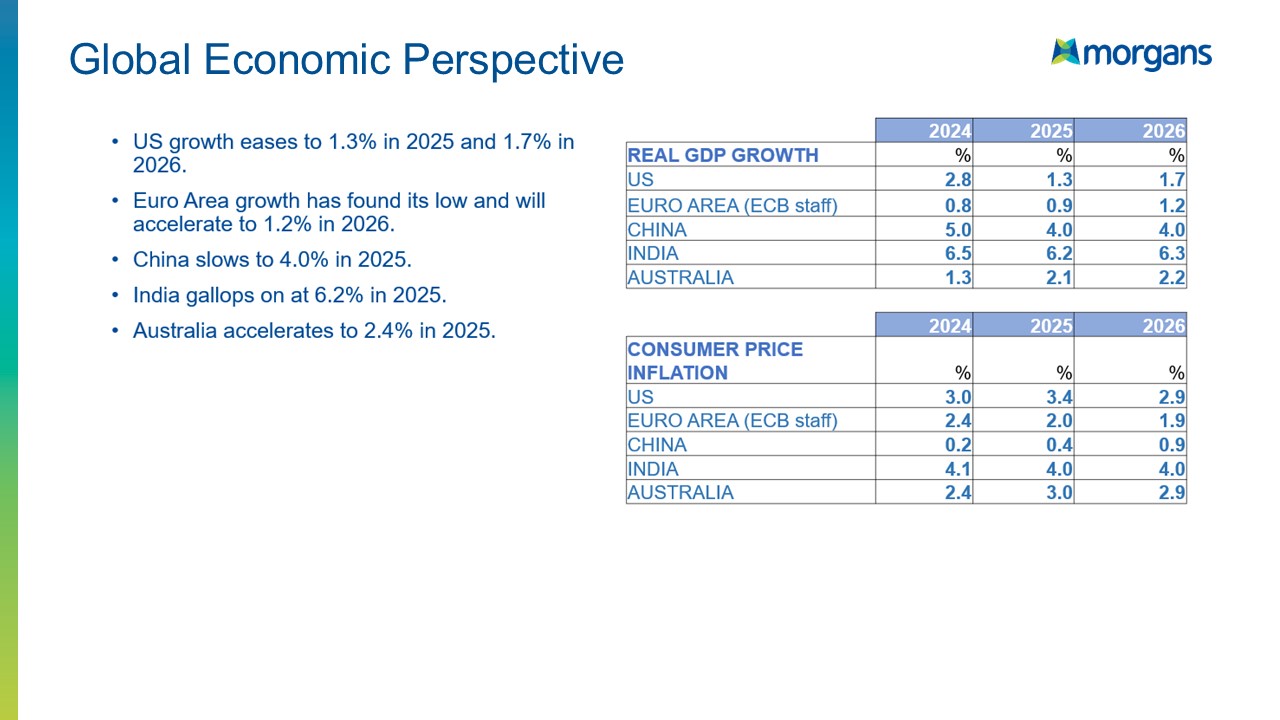

In my presentation today, I’m outlining the economic outlook for growth and inflation in the U.S., the Euro area, China, India, and Australia, drawing data from the International Monetary Fund, the Congressional Budget Office, European sources, and my own analysis for Australia.

For the U.S., the best-case scenario is a soft landing, with growth slowing but remaining positive at 1.3% this year and rising to 1.7% next year. This slowdown allows the Federal Reserve to continue cutting interest rates, leading to a decline in the U.S. dollar. This in turn ,triggers a recovery in commodity prices. These prices have stabilized and are now trending upward, with an expected acceleration as the dollar weakens.

U.S. headline inflation is projected to be just below 3% next year, with higher figures this year driven by tariff effects.

In the Euro area, growth is accelerating slightly, from just under 1% this year to 1.2% next year, with inflation expected to hit the 2% target this year and dip to 1.9% next year.

China’s GDP growth is forecast at 4% for both this year and next, a step down from previous 5% rates, reflecting a significant slump in domestic demand and very low inflation Chinese Inflation is only : 0.2% last year, 0.4% this year, and 0.9% next year. Despite a massive fiscal push, with a budget deficit around 8% of GDP, China’s debt-to-GDP ratio is rising faster than the U.S.. Yet this is yielding more modest domestic growth.

India, on the other hand, continues to outperform, with 6.5% GDP growth last year, 6.2% this year, and 6.3% next year, surpassing earlier projections.