The Wall Street Journal of 21 August 2025 carried an article which noted that Ether, a cryptocurrency long overshadowed by Bitcoin has surged in price in August.

The article noted that unlike Bitcoin, there was not a hard cap on Ether supply, but the digital token is increasingly used for transactions on Ethereum , a platform where developers build and operate applications that can be used to trade, lend and borrow digital currencies.

This is important because of the passage on 18 July 2025 of the GENIUS act which creates the first regulatory framework for Stablecoins. Stablecoins are US Dollar pegged digital tokens. The Act requires that Stablecoins , are to be to be fully backed by US Treasury Instruments or other US dollar assets .

The idea is that if Ethereum becomes part of the infrastructure of Stablecoins , Ether would then benefit from increased activity on the Ethereum platform.

Tokenized money market funds from Blackrock and other institutions already operate on the Ethereum network.

The Wall Street journal article goes on to note that activity on the Ethereum platform has already amounted to more than $US1.2 trillion this year ,compared with $960 million to the same period last year.

So today ,we thought it might be a good idea to try and work out what makes Bitcoin and Ether go up and down.

As Nobel Prize winning economist Paul Krugman once said " Economists don't care if a Model works in practice ,as long as it works in theory" . Our theoretical model might be thought as a "Margin Lending Model" . In such a model variations in Bitcoin are a function of variation in the value of the US stock market .

As the US stock market rises, then the amount of cash at margin available to buy Bitcoin also rises .

The reverse occurs when the US stock market goes down .

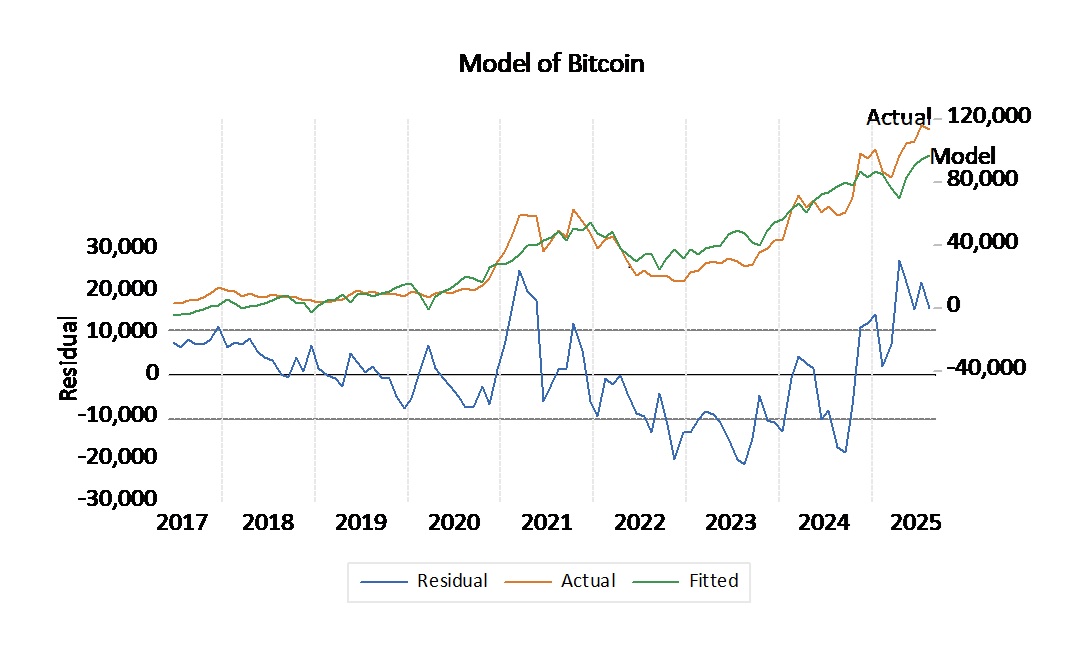

Our model of Bitcoin based on this theory is shown in Figure 1 . We are surprised that this simple model explains 88% of monthly variation in Bitcoin since the beginning of 2019.

At the end of August our model told us that when Bitcoin was then valued at $US112,491 , that it was then overvalued by $US15,785 per token.

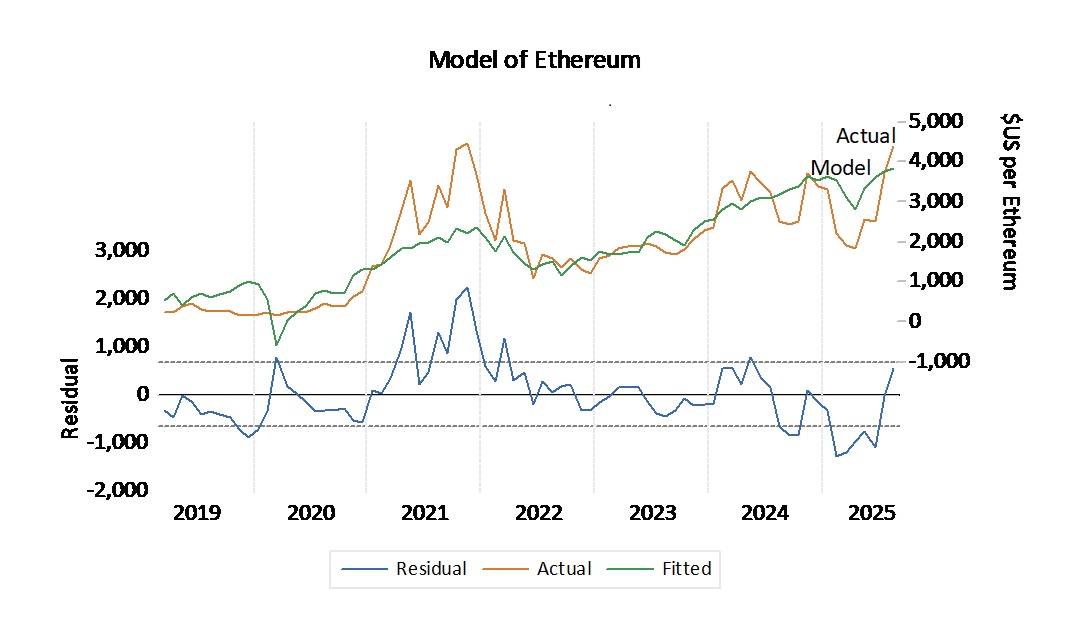

Modeling Ether is not so simple . Ether is a token but Ethereum is a business. this makes the price of Either sensitive to variations in conditions in the US Corporate Debt Market.

Taking that into account as well as stock market strength, gives us a model for Ether which is shown in figure 2.

This model explains 70.1% of monthly variation since the beginning of 2019. Our model tells us that at the end of August, Ether at $US 4,378per token was $US 560 above our model estimate of $US3,818.00 . Ether is moderately overvalued.

So neither Bitcoin nor Ether are cheap right now.

ETFs for each of Bitcoin and Ether are now available from your friendly local stockbroker .

But right now , our models tell us that neither of them is cheap!