- As attention turns to the August reporting season, earnings estimates appear to be on much shakier ground this time around. Soft trading updates from retailers in May/June have reinforced the view that the economy has reached a weaker period after months of enduring elevated inflation and higher interest rates.

- Quantity and quality of earnings will come into focus as the macro takes a back seat to company fundamentals. Key themes to watch include FY24 earnings trends, higher interest costs, cyclical signposts (consumer demand, industrial margins), small cap performance, short selling and positioning in resources.

- Morgans analysts preview the results for 145 stocks under coverage that report in August and call out likely surprise and disappoint candidates from page 9.

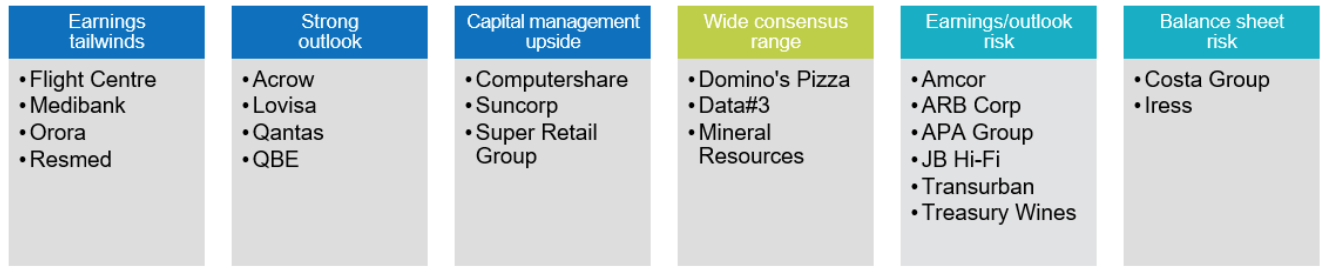

- Key tactical trades (page 2) include Resmed, Flight Centre, Orora, QBE, Medibank, and Lovisa among many others.

Watch

EPS erosion and not a collapse

FY24 EPS growth for ASX200 Industrials has slipped from 12% growth to c6% since February, and while this is a momentum headwind, this rate is only marginally below the 7% 20-year average EPS growth rate for ASX Industrials.

Corporate profit growth isn’t bad in a long-term Australian context. It just isn’t nearly as compelling as it has been through recent – post-pandemic – history. However, we explain why we think there will be some dividend restraint in August.

Much like the past few reporting periods, company outlook will be closely watched and we think the wide divergence of corporate performance will provide opportunities for tactical investors. We look for companies that are less prone to earnings erosion.

These include those with a growing earnings profile, strong cash flow profile and trading at reasonable valuations.

Balance sheets back in focus

As demand slows, the rapid rise in interest rates after a drawn-out period anchored at zero has renewed the focus on balance sheets and gearing. The decision to fix or hedge borrowing may buy companies some time but debt obligations can no longer be ignored with business lending costs rising from 1.5% in January 2022 to 5.2% in May 2023 (RBA, APRA).

Recent company updates have already called out higher interest costs as an earnings headwind in FY24: GNC, ORI, CKF, REITs. We expect financing costs to come under scrutiny. We think the most at risk include Amcor, Aurizon, Costa Group, Cromwell, Cleanaway, Domino’s Pizza, Star Entertainment Group and Wagners.

Key tactical calls around August results of interest

Morgans analysts identify key tactical calls around August results, where stock price reactions are flagged to surprise or disappoint. Insurers (QBE, Suncorp, Medibank and NIB) all enjoy momentum from higher investment yields, price rises and benign claims.

Rebounding travel demand supports for Qantas and Flight Centre where we see upside risk to FY24 expectations.

Consumer stocks have been under pressure, but we think results for the likes of Super Retail, Lovisa and Domino’s can re-ignite market interest. Watch also for potential weakness in a cross-section of larger names including Amcor, ARB Corp, Treasury Wines, Transurban and APA Group.

Figure 1: Tactical opportunities - Morgans reporting season surprise candidates

Morgans clients receive access to detailed market analysis and insights, provided by our award-winning research team. Begin your journey with Morgans today to view the exclusive coverage.