Last time I spoke to you about Australian inflation and its effect on what the RBA might do in its November meeting, I said that expectations for inflation for the year to September, which would be published in October, were between 2.5% and 2.7%. I also said that if inflation came in at the lower estimate of 2.5%, then we could see a rate cut in November.

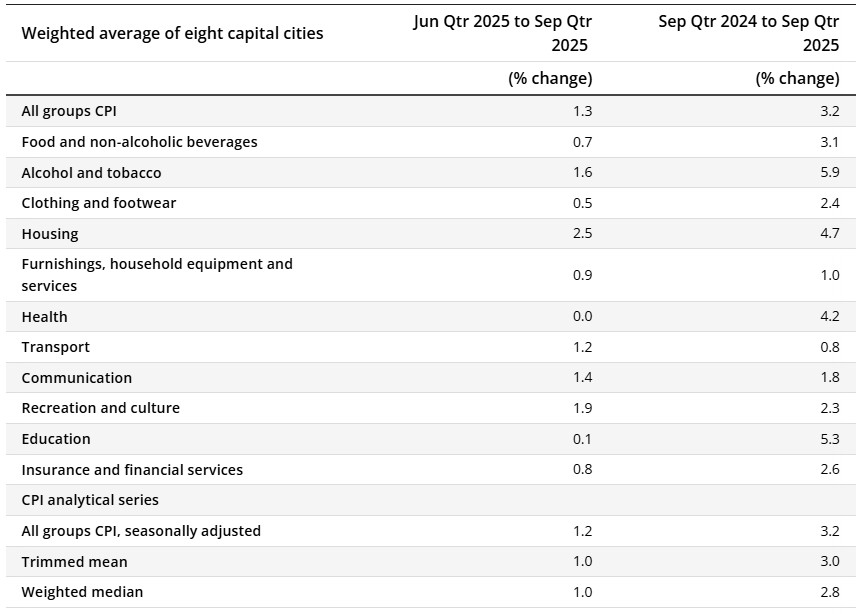

Well, the numbers are out, and unfortunately, not only are we not getting a rate cut in November, it’s unlikely we’ll see another rate cut any time soon. In fact, it’s fair to say we may be at the very end of the rate-cutting cycle in Australia. The reason is that the core measure, the trimmed mean, which is the RBA’s preferred measure of underlying inflation, came in not at 2.5%, not at 2.6%, and not even at 2.7%, but at a shockingly high 3%.

This result was driven by a 1.3% increase in prices in the previous quarter, which annualises to about 5%, a surprise that wasn’t anticipated. Looking deeper into the quarterly CPI, we saw housing prices rising at 4.7%, health costs up 4.2%, and education costs increasing by 5.3%.

The ABS has indicated that the major source of inflation was a jump in goods inflation, which rose 3%, up 1.1% from the previous quarter, or 4.4% annualised. The standout contributor was electricity, which saw a massive year-on-year increase of 23.6%. Other household fuels actually fell by 1.6%, and annual services inflation was 3.5%.

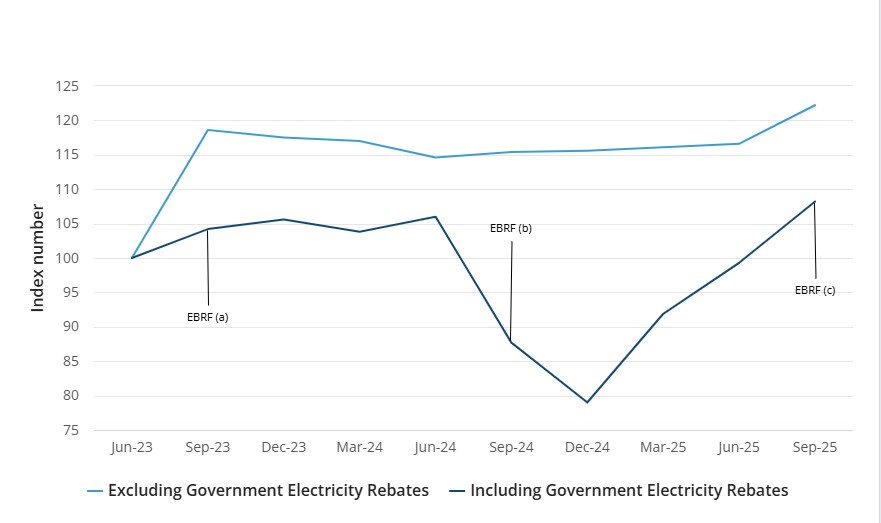

The ABS attributed this unexpected rise in inflation primarily to electricity prices. But it’s not just electricity prices themselves, it’s the end of Federal Government funding to the states that had been keeping those prices low.

The ABS reported that electricity prices rose 23.6% over the past 12 months, largely because State Government rebates, funded by the Commonwealth under the Energy Bill Relief Fund, have now been used up. These rebates included Queensland’s $1,000 rebate, Western Australia’s $400 rebate, and Tasmania’s $250 rebate. With these rebates exhausted, electricity prices have surged.

The ABS data shows electricity prices excluding government rebates, and highlights the impact of the federal funding. Electricity prices really took off in 2023, rising by almost 20%, which posed a political risk for the Federal Government. In response, the Government provided funding to State Governments to suppress those prices. There were schemes in both 2023 and 2024, and ahead of the last election, the subsidised price paid by consumers dropped to around 80% of the original cost, well below the actual cost of generation.

However, since December 2024, those subsidies have been reduced. Over the past year, prices have climbed again, though they remain below the unsubsidised cost, which is now around 122% of the original price, or about a quarter higher than where things stood in 2023.

The result of all this is 3% core inflation. If inflation had come in at 2.5%, rates could have fallen from 3.6% to 3.35%. But with 3% core inflation, rates should need to rise by 25 basis points. That said, we’re likely at the end of the rate-cut cycle.

Is the RBA likely to raise rates? They might consider it, but this is cost-push inflation, not demand-driven inflation, so increasing rates wouldn’t help. It would only worsen the situation. This very high inflation figure, driven by the end of federal electricity subsidies, signals the end of the current series of Australian rate cuts.