The war between the United States and Iran has generated major falls in world oil production this year.

The International Energy Agency, in its June report, suggested that global supply is set to fall by 3 million barrels a day, or by a total of 102 million barrels in 2026, before rebounding next year. In May, output declined to 94 million barrels a day, and that was down by 13.6 million barrels a day in comparison to the levels of production before the conflict.

While the US-Iran interim agreement paves the way for a rebound in Middle East exports, operational and political constraints, the IEA tells us, including prolonged de-mining efforts to remove sea mines that are blocking tankers and unresolved transit arrangements, leave a lot of downside risk to the outlook. Refinery crude throughput is forecast to contract by 2 million barrels a day to 82 million barrels a day in total, led by a 4.7 million barrel decline in the second quarter alone in 2026.

So, notwithstanding the interim peace deal, 2026 crude runs are estimated to be cut by 370,000 barrels a day, reflecting much deeper cuts in the third quarter. In China, the Middle East, Eurasia and non-OECD economies, refinery runs are expected to rebound only in 2027. What this means is that we are seeing a decline in global inventories of oil and refined products.

In May, we saw a decline of a total of 143 million barrels, or 4.6 million barrels a day, which was much greater than the 74 million barrel decline recorded in April. That means that by the middle of next quarter, the IEA estimates inventories will have fallen by around 163 million barrels.

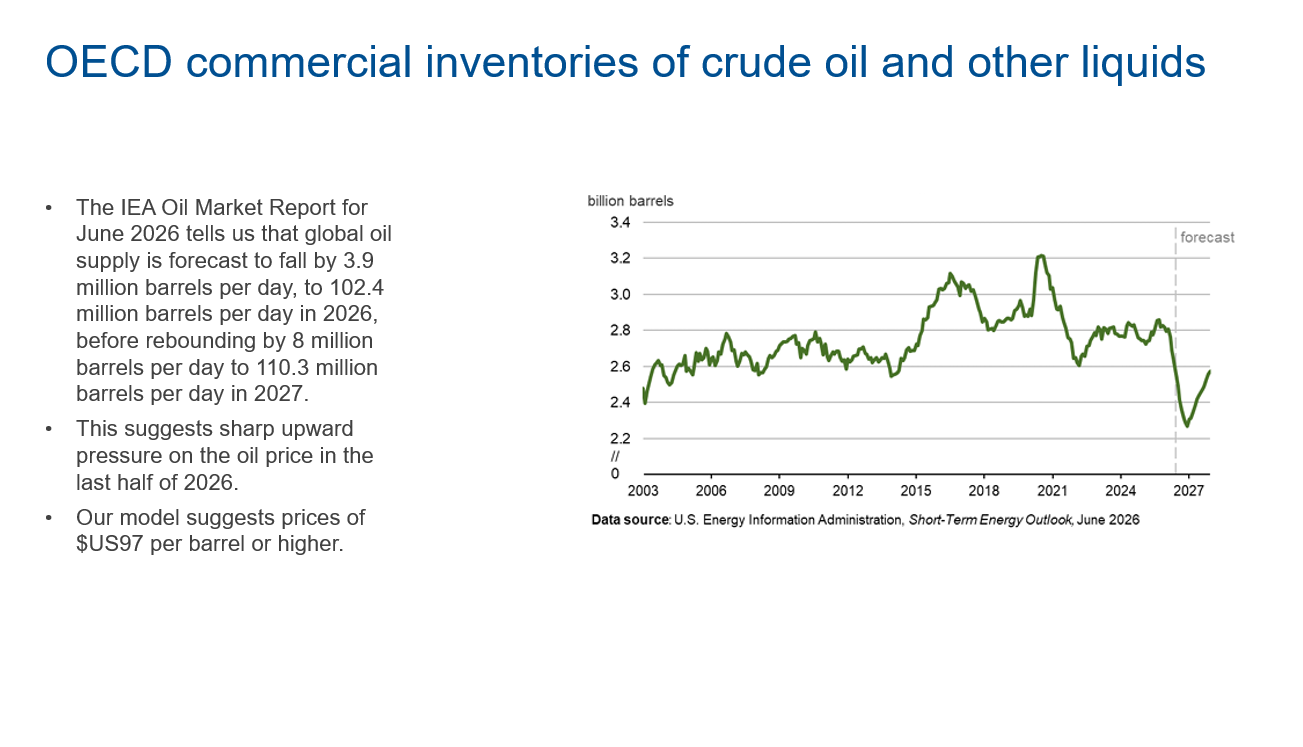

The OPEC market report for June tells us that global oil supply is forecast to fall by 3.9 million barrels a day to 102 million barrels a day in 2026 before rebounding by 8 million barrels a day next year. The problem is that when we look at the chart of OECD commercial inventories of crude oil and other liquids, what we see is a very dramatic fall in the quarter immediately ahead of us.

That fall does not turn around and begin to improve. In fact, there is no improvement in inventories forecast before the first half of 2027. When we model oil prices, what we see is that the level of inventories, or stocks on hand, is usually the largest single driver of the price. Therefore, we think the decline in the oil price seen so far is getting a bit ahead of itself and is only being supported by additional oil supplied from the US Strategic Petroleum Reserve and China's strategic reserves.

We think that this decline in oil price is unsustainable. By the time we get into the second half of this year, particularly around September and October, inventories will be significantly lower, and that will drive prices higher than they currently are.

Our modelling of the Brent crude price suggests that it will rise back to US$97 a barrel before the end of the year.

Want to discuss how this impacts your portfolio?

DISCLAIMER: Information is of a general nature only. Before making any financial decisions, you should consult with an experienced professional to obtain advice specific to your circumstances.